The story of Optionsellers ~$150mil blowup

The story of Optionsellers ~$150mil blowup

Blowing up selling options

This has been the decade of options.

While stock volume has increased over the past years, options truly took over, boosted by the 2020 mania and fueled by new brokerage options, making it easy for beginners to dabble in the markets.

Trading in options, as depicted by the volume, surged 478% in the past decade.

As traders and institutional players look for alpha, market makers made it their mission to provide adequate market making and thus volume on any optionable asset.

On the other side of long-only option traders and market makers, a new kind of trading and search of returns led a certain kind of investor to explore the world of option selling.

In contrary to the limited risk for buy-only investors within the option market, the sellers pocket in a premium and assumes the risk above or below the strike. Similar to shorting, the risk becomes almost unlimited.

This dynamic is what we will discuss in this paper, which will go over one of the most publicized blowup from 2018, the Optionsellers fund blowup.

James Cordier's Early Career and Rise to Success

James Cordier grew up in Sturgeon Bay, Wisconsin as one of six children of a police officer. After graduating from high school in 1980, he went to work at Sears and took some commodities trading classes, though the specific details of his early education are unclear.

He began his career as a retail broker in the 1980s and 90s, developing a specialty in the fundamentals of physical commodities such as softs, grains, metals, and energies. In the 2000s and 2010s, Cordier parlayed this commodity market expertise as a Commodity Trading Advisor (CTA), becoming better known as an options strategist and trusted voice in national financial media. During this time, he served as a licensed commodity futures broker, portfolio manager, and head of the Milwaukee branch office for Allendale, Inc. from 1990 to 1999.

Cordier went on to become a successful options trader. He founded his own company, OptionSellers.com, which catered to wealthy clients such as Tampa Bay Lightning owner Jeff Vinik.

Cordier was considered a "genius" at trading options and had written books on the specific topic of options selling, appearing on cable TV to share his expertise.

His deep knowledge of physical commodities and options trading strategies, combined with his self-confidence and media presence, allowed him to attract a wealthy client base, including Tampa Bay Lightning owner Jeff Vinik.

Cordier's company OptionSellers.com had nearly "blown up" once before due to its connection to a brokerage whose CEO was imprisoned for embezzling over $200 million from clients' accounts.

The $150mil blowup

After two decades of sucessful trading, the end of the OptionSellers fund would come.

Option Sellers, LLC was a Tampa, Florida-based Registered Investment Adviser and CTA. They managed money for 290 clients. The minimum investment was $250,000, however most investors likely had additional capital given the 150mil damage that led to the closure of the fund.

In the autumn of 2018, the Bureau of Labor Statistics (BLS) revealed that the supply of natural gas stored hit its lowest level in 16 years. Fast forward to November 14th, 2018, and concerns over a looming cold front caused a sharp spike in natural gas futures, surging by 18% to reach a four-year high on that day, as depicted in the chart above.

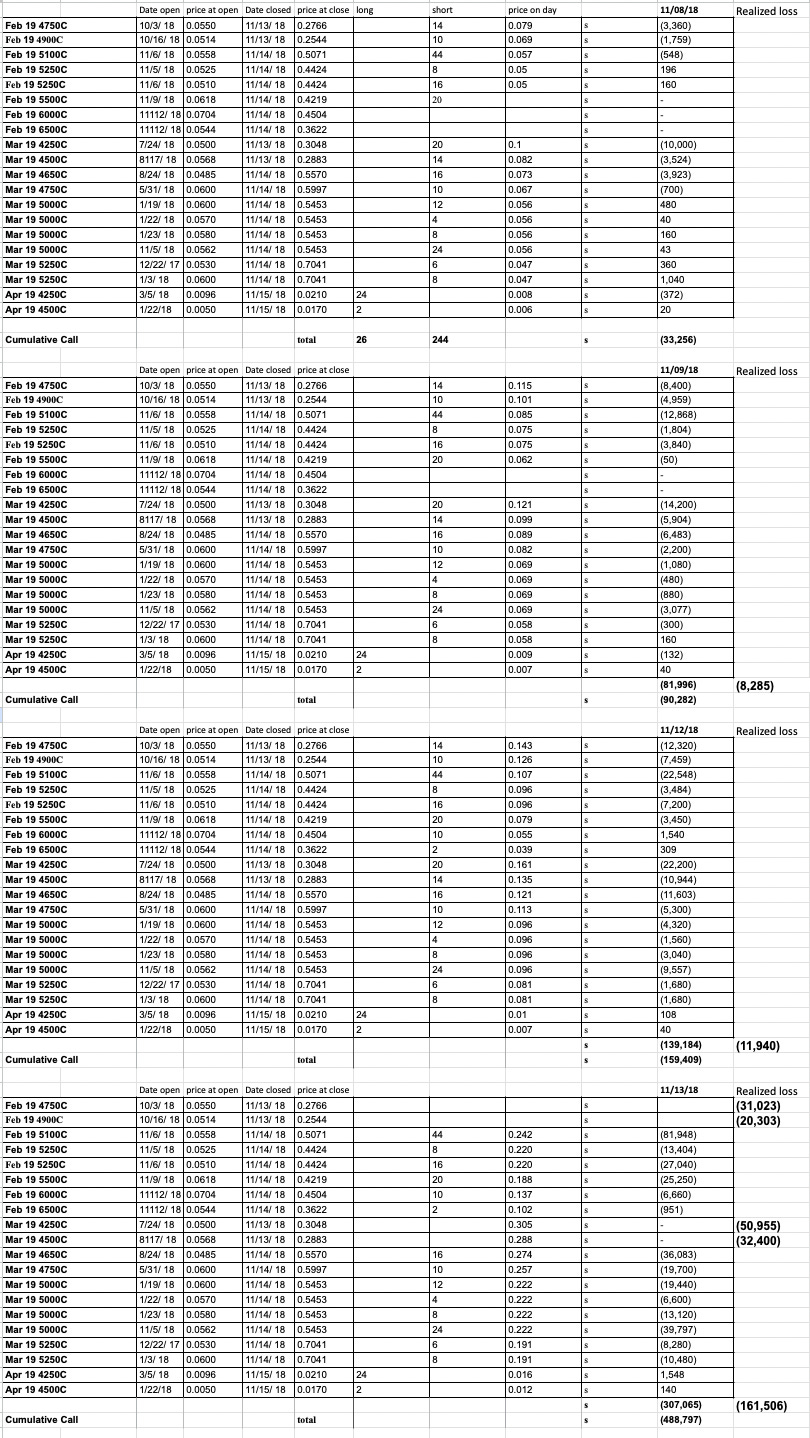

The Optionsellers fund had taken substantial short positions in calls. This decision triggered a chain reaction wherein these short positions needed to be covered due to the perceived risk, all within the span of Thursday, November 8th 2018 until Tuesday 13th. Consequently, when James failed to provide collateral for the margin call, his broker, INTL FCStone, liquidated his positions, resulting in a realized loss of $150 million.

Not only did investors suffer a complete loss of their investment, but they were also confronted with margin debt calls amounting to approximately one-third of their initial investment, leaving many clients on the hook to settle trade balances, according to legal filings.

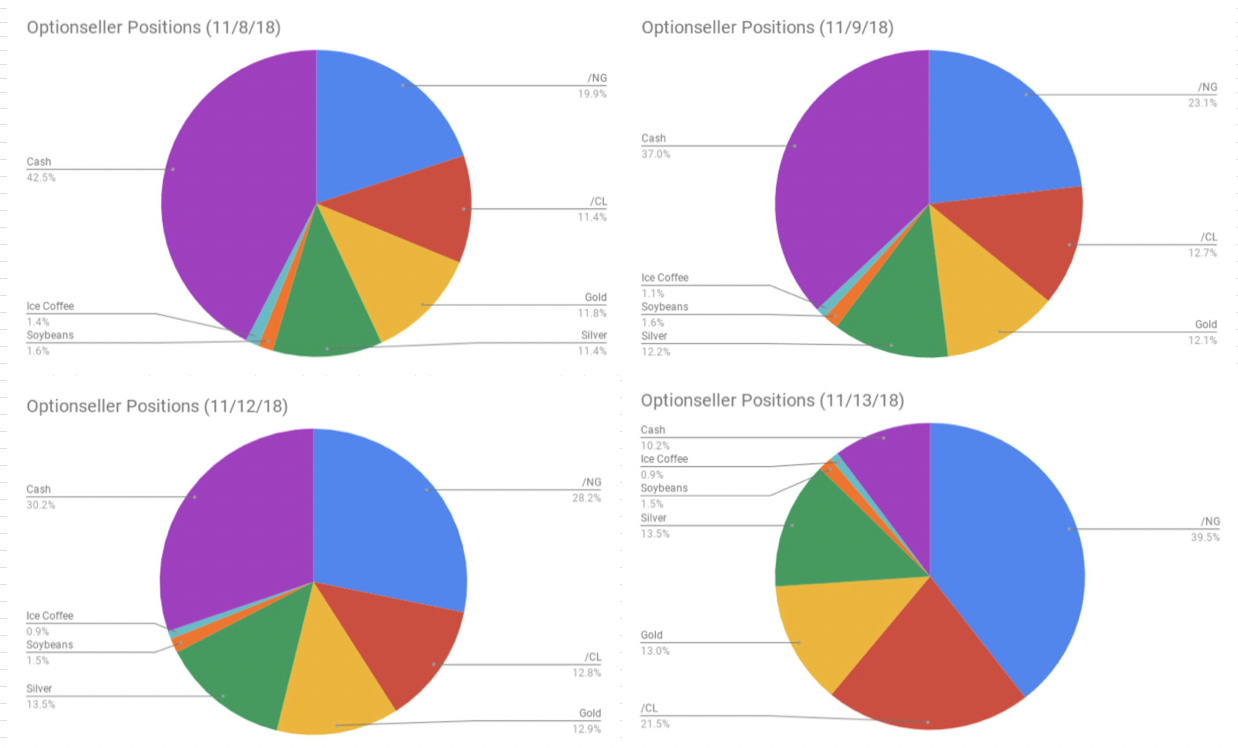

The portfolio

One specific investor posted the specific trades the fund had on at the time of the events and provided these for us all to learn from. The investor had invested $400K and within a week, the invested capital loss grew to over -$1,000,000. (this explains the lawsuits and brokerage involvement in this matter)

Using his individual positions as a percentage of the overall portfolio, we can reconstruct the funds loss.

As depicted below, the portfolio seemed somewhat balanced, but focused on Natural Gas, which constituted 19.9% of the portfolio. Within four days the size of the bet more than doubled through the adverse move, squeezing the cash position and ultimately leading to a large margin call.

The Natural gas bet was build as a strangle, yet the long call position was about 10 time smaller than the short call position, effectively leaving the fund exposed to a large move. As the underlying asset increased towards the deep out of the money call, the delta as well as the implied volatility (vega) increased, exponentially growing the loss as the calls repriced higher.

A peculiarity about these events is the contradicting nature of the trade, as James Cordier seemed to have the knowledge not to sell calls on natural gas during that time of the year. Based on his own book, and seasonal averages, gas as a commodity is expected to rise in the fall and peaks usually around jan-feb, which would have been a more prudent time to sell calls.

110 ex-investors out of the 290 individuals started a legal campain against Cordier, his company, and broker-dealer INTL FCStone.

The loss simply exponentially grew as we got closer to strike price while expanding the volatility drastically.

Shortly after the events unfolded, James Cordier released the following video, apologizing to his investors. The lawsuits continued in the background, and communication with the outside world stopped until James Cordier created his new company, Cordier Commodity Report (CCR).

Founded in 2021, CCR was established to provide expert fundamental analysis to professional traders and portfolio managers. In 2023, CordierCommodityReport.com was launched as a free and independent resource for all investors. James personally oversees every aspect of the business, maintaining a hands-on approach to research and analysis.

This past year, an increasing amount people I work with started to short options as a means to create alpha. This blog was a project I wanted to work on to display the risks linked to this type of approach. The leverage effect of options and the greeks make it easy to under-appreciate the risk while time in the game makes the black swan increasingly likely.

Personally, selling options to me is an option I would consider in two scenarios.

Selling calls against an existing long common stock position to close out a part of my position while pocketing the premium. I am effectively hedged while getting paid for it. This only works if I accept the risk of an asset continuing higher, but that is the same for selling a partial.

Selling puts as an attempt to be exercised at a discount, while creating passive cash flow in the meantime. This entails the risk of a potential sudden gap down in the asset I am trying to buy, which means the only size I would consider selling puts with would equal the desired long term position as if I had held shares long overnight.

95% of investors or traders I have talked to about being under pressure through sold options simply sold too many options and did not see them as potential real shares of a business.

Great read Lukas!

Good post. I founded an options market making firm in 2017. Would love to touch base and share some experiences.