Today I wanted to dig into Howard Marks, an investor known for his expertise in distressed debt and high-yield bonds. Howard marks is known through Oaktree Capital Management which he co-founded in 1995 and became one of the largest distressed debt investors in the world. Oaktree's 17 distressed-debt funds (which do not use leverage) have averaged annual gains of 19% after fees from the inception until 2020.

The Most Important Thing is a book that summarizes a collection of memos written by Howard Marks to his clients throughout the years. The book summarizes his investment philosophy and key beliefs he uses to operate on a daily basis and reflect on the market place.

This blog will go through each chapter and explain the key points Howard Marks tried to make. Hopefully each investor can learn and reflect on their own processes and perhaps even adding new parts through these shared lesson.

Second-Level Thinking

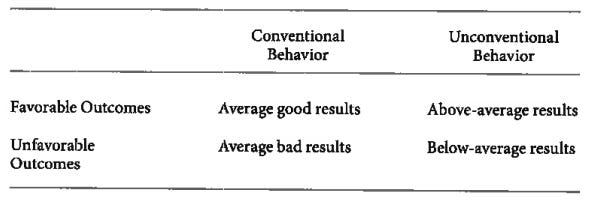

Investing is a complex art form that cannot be routinized, and even the best investors do not get it right all the time due to the uncontrollable environment and the variability of psychology. Successful investing requires thinking at a higher level and finding an edge that others do not have. If most investors underperform, one must do what most do not. This is where second-level thinking comes in, which involves thinking differently from others to achieve better-than-average results.

SETH KLARMAN: Beating the market matters, but limiting risk matters just as much. Ultimately, investors have to ask themselves whether they are interested in relative or absolute returns. Losing 45 percent while the market drops 50 percent qualifies as market outperformance, but what a pyrrhic victory this would be for most of us.

The following are the key points discussed in this chapter:

Investing is about achieving more than market returns and requires patience, good luck, or superior insight.

To achieve superior investment results, one must hold non-consensus views regarding value, and they have to be accurate.

Exceptional analytical ability, insight, or foresight is required to consistently achieve superior investment returns, which is a rare trait.

Second-level thinking is essential for successful investing, as it helps investors find an edge that others do not have.

The prevalence of first-level thinkers increases the returns available to second-level thinkers.

Above-average profits are not found by agreeing with the broad consensus.

Overall, second-level thinking is crucial for successful investing. It requires going beyond the conventional wisdom and thinking differently to identify unique investment opportunities that can generate above-average returns

CHRISTOPHER DAVIS: The subtext here is that you must be patient and give yourself ample time—you’re not looking for short-term windfalls but for long-term, steady returns.

Understanding Market Efficiency

The Efficient Market Hypothesis (EMH) is a theory of finance that posits that markets are efficient, and prices already reflect all available information. However, this theory does not imply that the market is always right, and asset prices can still be misvalued despite being efficient.

SETH KLARMAN: Psychological influences are a dominating factor governing investor behavior. They matter as much as—and at times more than—underlying value in determining securities prices.

Most of these characteristics are not permanent. Something broadly accepted can become controversial or even taboo. Information can become more or less available. Thus, an asset class deemed close to efficient at one point may become quite inefficient at another. European sovereign debt is a current example of this.

Key Points:

The EMH suggests that it is difficult for one person to hold a view that is different from the consensus and closer to being correct due to psychological influences that affect investor behavior.

The theory assumes that thousands of rational and objective people analyzing an asset can evaluate it diligently, making it challenging to beat the market.

However, some asset classes can be inefficiently priced based on different factors like their level of acceptance, availability of information, and comprehensibility.

To achieve superior results, second-level thinkers depend on inefficiency, looking for instances of misperception or mistakes that can be taken advantage of.

Silos or narrow focuses in specific market niches may lead to superior knowledge but also leave a strong possibility of mispricings outside those borders.

An asset class deemed close to efficient at one point may become quite inefficient at another.

JOEL GREENBLATT: This is very important and helps explain why most professionals have a hard time beating the market. Investments that are out of favor, that don’t look so attractive in the near term, are avoided by most professionals, who feel they need to add performance right now.

The chapter emphasizes the importance of estimating the intrinsic value of an asset and fundamental analysis in successful investing.

JOEL GREENBLATT: Warren Buffett says that the best investment course would teach just two things well: How to value an investment and how to think about market price movements. Step one starts right here.

This estimate of value includes an estimate for future growth in earnings or cash flow.

One of Buffett’s major contributions has been to extend the idea of value beyond the simply “cheap.” Buffett looks for “good” businesses that are available at an attractive price. The concept of growth is incorporated into the calculation of value

Key points include:

The starting point for successful investing is estimating the intrinsic value of an asset.

Fundamental analysis is the most effective method for determining intrinsic value.

Technical analysis and momentum investing are less useful approaches to investing.

Value investing and growth investing are the two primary approaches based on fundamentals.

Value investors aim to identify an asset's current intrinsic value and buy when the price is lower, while growth investors try to find securities that will increase in value over time.

Value investing centers on consistency and has the potential for more consistent returns.

The margin of safety is essential in investing to mitigate risk.

Investors must be patient and have a long-term perspective to realize success.

While growth investing focuses on big winners, value investing emphasizes the importance of accuracy in estimating value and consistency in returns.

The chapter highlights the need for investors to be prepared for the possibility of being wrong or looking wrong in the short term and the importance of a margin of safety in investing.

The Relationship between Price and Value

The key to successful investing is not just buying good things but buying them well. The relationship between an asset's value and its price is crucial to successful investing. Thus, it is essential to keep in mind that an asset's price should converge with its intrinsic value over time.

The most dependable way to make money in investing is by buying something for less than its value and having the asset's price move toward its value over time. However, buying cheap is not a guarantee for success and can be affected by events that reduce value or market deterioration.

CHRISTOPHER DAVIS: Investors should be wary of the risk of obsolescence, which can turn a cheap stock into a value trap.

To succeed, investors must estimate the intrinsic value of an asset using fundamental analysis. They should consider the fairness of an asset's price before deciding to invest. This approach requires patience and a long-term perspective to realize success.

JOEL GREENBLATT: Individual investors need to think of this “most important” point with every investment decision. No matter how good an investment sounds, if price has not yet been considered, you can’t know if it is a good investment.

Finally, it's important to have a strong view of intrinsic value to help with conviction and to hang in until the market comes to agree with the investor.

JOEL GREENBLATT: Once again, as Buffett would say, the best investment class would teach how to estimate value and then how to think about market prices. Merely understanding that prices can deviate wildly from value over the short run is key. Understanding psychology so that you can take advantage of these deviations when they appear is the hard part

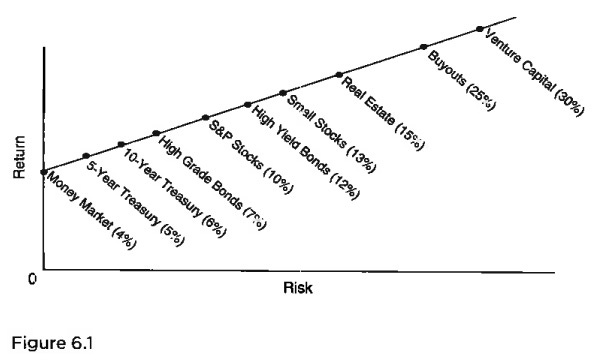

Understanding Risk

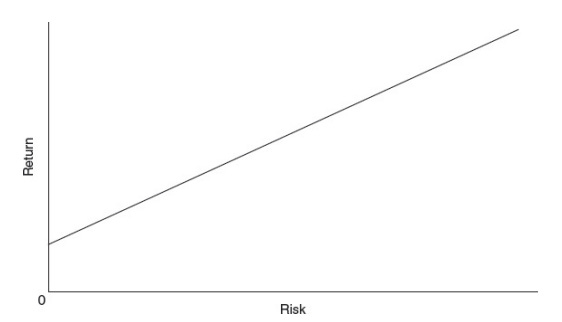

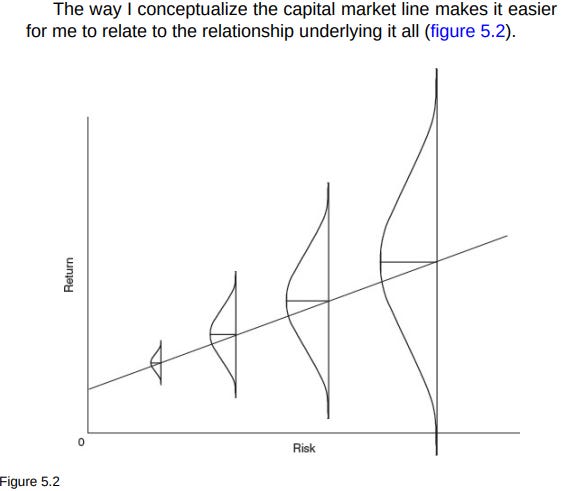

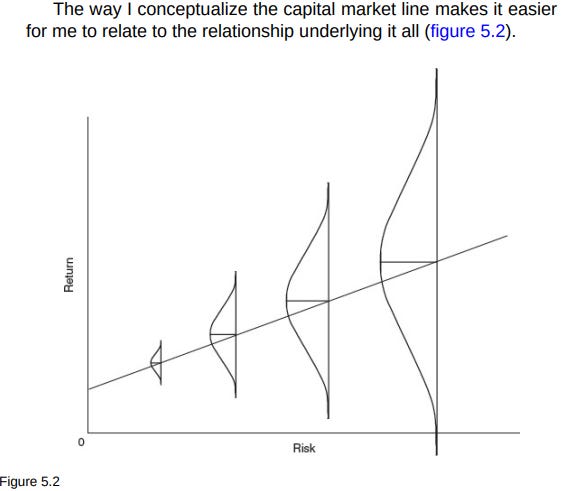

Investment decisions require a careful assessment of risk. Investors need to consider the potential return and the risk entailed before making a decision. The risk-return relationship is positive, but it doesn't mean that riskier investments will always deliver higher returns. The uncertainty of the future makes risk assessment difficult, and investors must fashion a probability distribution to weigh the possibilities. The most significant risk that investors worry about is permanent capital loss, but other risks such as underperformance, career risk, unconventionality, and illiquidity can also affect investments. Investors may also overlook high risks in search of high potential returns, leading to loss.

‘Surely investors who get their statements and find that their accounts made 10 percent for the year don’t know whether their money managers did a good job or a bad one. In order to reach a conclusion, they have to have some idea about how much risk their managers took. In other words, they have to have a feeling for “risk-adjusted return.”

:However, many individual and institutional investor decisions are based on this number, which has little explanatory or predictive value.’

JOEL GREENBLAT

Main points:

Risk is an essential element in the investment process, and investors must assess the potential return and the risk entailed before making a decision.

The risk-return relationship is positive, but riskier investments cannot be counted on to deliver higher returns.

Understanding the uncertainty of the future is crucial to assessing risk.

Investors face different types of risks such as permanent capital loss, underperformance, career risk, unconventionality, and illiquidity.

Investors may overlook high risks in search of high potential returns, leading to loss.

Investors must fashion a probability distribution to weigh the possibilities and calculate the expected result.

The normal distribution was an important contributor to the 2008 financial crisis as people made assumptions that future events would be normally distributed

Recognizing risk

In this chapter, Howard Marks emphasizes the importance of recognizing and managing risks in investing, as high risk often comes from high prices that increase the likelihood of loss. The relationship between price and value is a crucial factor in dealing with risk, and investors should demand risk premiums for bearing incremental risk. In upswings, risk increases as financial imbalances build up, and materializes in recessions. Investors who aren't sufficiently risk-averse may pay prices that are too high, leading to losses.

HOWARD MARKS: The riskiest things: The greatest risk doesn’t come from low quality or high volatility. It comes from paying prices that are too high. This isn’t a theoretical risk; it’s very real

CHRISTOPHER DAVIS: High price both increases risk and lowers returns.

Takeaway:

High risk comes from high prices, which increase the likelihood of loss.

The relationship between price and value is a crucial factor in dealing with risk.

Investors should demand risk premiums for bearing incremental risk.

Risk increases as financial imbalances build up, and materializes in recessions.

Investors who aren't sufficiently risk-averse may pay prices that are too high, leading to losses.

Risk premiums have been decreasing due to investors' willingness to take on riskier investments and low interest rates.

This behavior creates a high-risk environment and could lead to a market meltdown.

Investors should be aware of the current investment environment and the risks involved.

The 2008 financial crisis highlights the need for investors to understand the risks they are taking on.

HOWARD MARKS: The riskiest things: “There are few things as risky as the widespread belief that there’s no risk.” The opening words of this paragraph are valuable because they highlight an excellent example of the ways investors’ behavior creates the risks to which they are subjected. When they swallow worry-free beliefs, it truly is the riskiest thing.

Controlling Risk

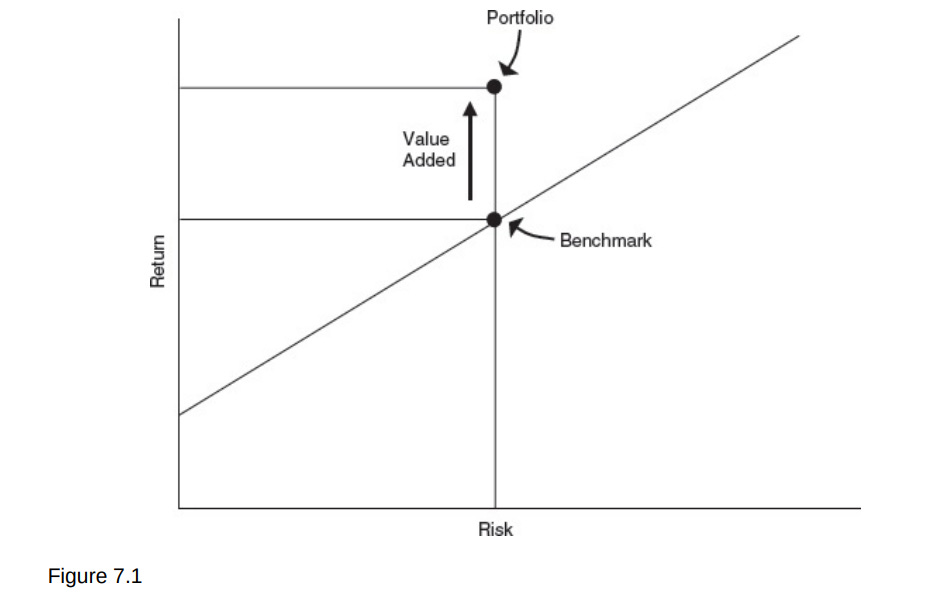

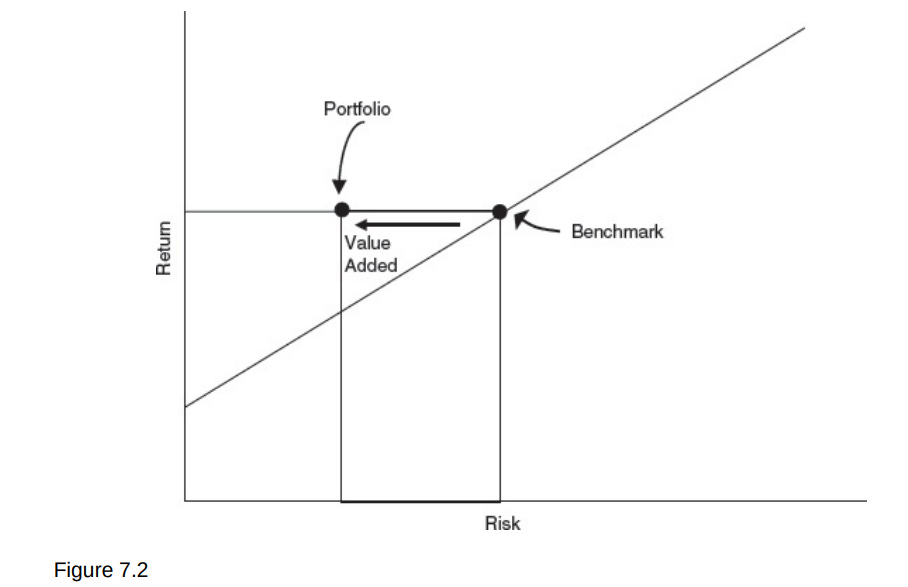

The chapter emphasizes the importance of controlling risk in investing and separating successful investors from the rest. It highlights the difficulty in assessing risk, particularly in worst-case scenarios, and notes that a skilled investor can achieve the same returns as a benchmark while taking less risk. The author acknowledges that there is no easy answer when it comes to preparing for unlikely disasters in investing.

Alpha can both be created through more returns per risk unit or less risk per return.

PAUL JOHNSON: Controlling the risk in your portfolio is a very important and worthwhile pursuit. The fruits, however, come only in the form of losses that don’t happen. Such what-if calculations are difficult in placid times. This is the ultimate paradox of risk management.

JOEL GREENBLATT: The math behind the compounding of negative returns helps ensure this outcome (e.g., a 40 percent loss in one year requires a return of 67 percent to fully recover)

Investors think about this tension between risk and reward in conjunction with the probabilities of each. One way to maximize the asymmetry of risk and reward is to make sure you minimize risk. I’ve said this before in another place: if you minimize the chance of loss in an investment, most of the other alternatives are good.

Important points:

Risk control is crucial for successful investing, but often less appreciated than high absolute returns.

Achieving high returns with high risk means little unless the risk is well-managed over many years.

Skilled investors can achieve the same returns as a benchmark while taking less risk, which is a great accomplishment.

Assessing an investor's investment process is more important than analyzing returns relative to a benchmark.

It's difficult to assess risk, particularly in worst-case scenarios, but investors should be prepared for once-in-a-generation events.

There is no easy answer when it comes to preparing for unlikely disasters in investing.

PAUL JOHNSON: Marks is clear in his distinction. Risk control is not risk avoidance, and the “right price” is the operative part of his statement.

Being attentive to Cycles

In this chapter, Howard Marks emphasizes the importance of recognizing the cyclical nature of almost everything, including investing. He suggests that investors can hold two concepts with confidence: that most things will prove to be cyclical and that some of the greatest opportunities for gain and loss come when others forget this rule.

JOEL GREENBLATT: Understanding that cycles are eventually self-correcting is one way to maintain some optimism when bargain hunting after large market drops.

Key takeaways from this chapter include:

Trees don't grow to the sky, and few things go to zero

Most things will prove to be cyclical

Opportunities for gain and loss come when others forget the rule of cyclicality

The credit cycle is inevitable, extremely volatile, and has the power to create opportunities for investors attuned to it

Understanding the cyclical nature of the economy can help investors maintain optimism during market drops

Oversupply leads to a price decline and lower profits, and investors will overvalue companies during good times and undervalue them when things get difficult

It is dangerous to believe that cyclicality has been ended, as the past repeats itself, and it is essential to recognize this error when it arises

HOWARD MARKS: The riskiest things: When things are going well, extrapolation introduces great risk. Whether it’s company profitability, capital availability, price gains, or market liquidity, things that inevitably are bound to regress toward the mean are often counted on to improve forever

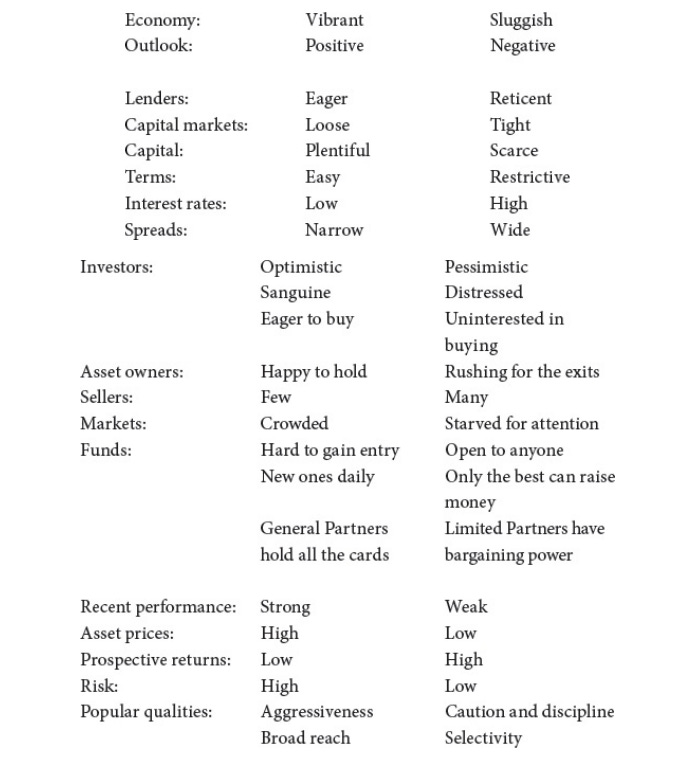

The chapter discusses the pendulum-like oscillation of investor attitudes and behaviors in the investment world, where investment markets swing between euphoria and depression, overpriced and underpriced, greed and fear, optimism and pessimism, credulousness, and skepticism. The swing in attitudes towards risk is a common thread that runs through many of the market's fluctuations, and improper amounts of risk aversion are key contributors to market excesses of bubble and crash.

HOWARD MARKS: The riskiest things: The ultimate danger zone is reached when investors are in agreement that things can only get better forever. That makes no sense, but most people fall for it. It’s what creates bubbles—just as the opposite produces crashes

Key Points:

The swing in attitudes towards risk is a common thread that runs through many of the market's fluctuations, and improper amounts of risk aversion are key contributors to market excesses of bubble and crash.

Investors should balance the risk of losing money and the risk of missing opportunity.

At the extremes of the pendulum's swing, one of these risks predominates, and investors may behave too aggressively or too conservatively.

Major investment opportunities occur at the bottom of the pendulum swing when everyone has given up hope.

Patience is important in waiting for value opportunities, as markets always create opportunities.

The pendulum-like pattern in most market phenomena can be both dependable and unpredictable.

The author outlines three stages of a bear market, with the third being the ultimate danger zone. The chapter emphasizes that major investment opportunities occur at the bottom of the pendulum swing when everyone has given up hope. The author highlights the importance of patience in waiting for value opportunities, as markets always create opportunities. The chapter ends with a discussion of the pendulum-like pattern in most market phenomena and how this pattern can be both dependable and unpredictable.

JOEL GREENBLATT: This means markets will always create opportunities, whether now or later. In markets with few opportunities, it’s important to be patient. Value opportunities will eventually present themselves, usually after no more than a year or two.

Combating Negative Influences

The chapter discusses the psychological factors that can influence investing decisions, including greed, fear, self-deception, and irrational decision-making. To consistently outperform in investing, it is essential to exploit inefficiencies caused by these psychological factors. However, investors must also combat negative influences such as conforming to the herd's view, envy, and ego. The greatest formula for long-term wealth creation emphasizes qualities such as awareness of what one doesn't know, humility, prudence, and risk control.

HOWARD MARKS: Emotion and ego: Psychological influences have great power over investors. Most succumb, permitting investor psychology to determine the swings of the market. When those forces push markets to extremes of bubble or crash, they create opportunities for superior investors to augment their results by refusing to hold at the highs and by insisting on buying at the lows. Resisting the inimical forces is an absolute requirement.

The chapter also highlights Howard Marks' warning about the tech bubble in 2000. Despite the appreciation of tech stocks, investors ignored the fact that not all companies could win and that shares in money-losing companies carried great danger. The tech bubble burst soon after, and greed, excitement, illogicality, suspension of disbelief, and ignoring value cost people a lot of money. To avoid such mistakes, investors must remain vigilant and maintain a disciplined approach to investing.

HOWARD MARKS: Emotion and ego: A lot of the drive in investing is competitive. High returns can be unsatisfying if others do better, while low returns are often enough if others do worse. The tendency to compare results is one of the most invidious. The emphasis on relative returns over absolute returns shows how psychology can distort the process.

SETH KLARMAN: Even the best investors judge themselves on the basis of return. It would be hard to evaluate yourself on risk, since risk cannot be measured. Apparently, the risk-averse managers of this endowment were disappointed with their relative returns even though their risk-adjusted performance was likely excellent, as borne out by their performance over the following three years. This highlights just how hard it is to maintain conviction over the long run when short-term performance is considered poor.

JOEL GREENBLATT: This is incredibly important. Most institutional and individual investors benchmark their returns, and therefore most end up chasing the crowd: accent on the wrong sylLABle.

A strongly held sense of intrinsic value, without it, an investor has no home base. A strong sense of intrinsic value is the only way to withstand the psychological influences that affect behavior. Those who can’t value companies or securities have no business investing and limited prospects (other than luck) for investing successfully. This sounds simple, but plenty of investors lack it.

Contrarianism

In this chapter, Howard Marks discusses the importance of contrarian investing for successful portfolio management. He argues that following the crowd does not guarantee success and that superior investors think differently from others. To avoid being part of the herd, investors must do the opposite of what others do. This requires complex and insightful analysis, also known as second-level thinking.

Marks emphasizes that market extremes are created by what most people believe, which means that the majority of people are wrong at these inflection points. Therefore, contrarian investors can profit by diverging from the crowd. The key to successful investing is to be skeptical and contrarian, going against the herd mentality of buying high and selling low.

JOEL GREENBLATT: I love this thought. Extreme circumstances (or, more accurately, opportunities) occur more often than seems reasonable. You never catch the bottom or the top of these situations, and that’s where the pain and degree of difficulty come in!

One of Buffett’s and Marks’s greatest concepts. In the long run, the market gets it right. But you have to survive over the short run, to get to the long run.

To do this, investors must have the ability to detect instances in which prices have diverged significantly from intrinsic value, experience, patience, and a strong stomach to defy conventional wisdom. Skepticism requires both pessimism when optimism is excessive and optimism when pessimism is excessive. The best investments are often uncomfortable and challenging, but they offer great potential for profit.

SETH KLARMAN: This is where it is particularly important to remember the teachings of Graham and Dodd. If you look to the markets for a report card, owning a stock that declines every day will make you feel like a failure. But if you remember that you own a fractional interest in a business and that every day you are able to buy in at a greater discount to underlying value, you might just be able to maintain a cheerful disposition

Marks argues that waiting for uncertainty to be resolved before buying can mean missing out on great bargains. Buying when everyone else is selling, based on a view of intrinsic value, can lead to the greatest rewards with the least risk. The article discusses the skepticism required during the global credit crisis of 2007-2008, and emphasizes that successful investing requires seeing some quality that others don't see or appreciate and having it turn out to be true.

HOWARD MARKS: Fear of looking wrong: The very words used here—uninstitutional, idiosyncratic, imprudent, lonely, and uncomfortable—provide an idea of how challenging it is to maintain nonconsensus positions. But doing so is an absolute must if superior performance is to be achieved.

Key points:

Contrarian investing is essential for successful portfolio management

Superior investors think differently from others and engage in second-level thinking

Market extremes are created by what most people believe, which means that the majority of people are wrong at these inflection points

The key to successful investing is to be skeptical and contrarian, going against the herd mentality of buying high and selling low

Waiting for uncertainty to be resolved before buying can mean missing out on great bargains

Buying when everyone else is selling, based on a view of intrinsic value, can lead to the greatest rewards with the least risk

Finding Bargains

In this chapter of "The Most Important Thing," Howard Marks discusses the process of intelligently building a portfolio. He emphasizes the importance of buying the best investments, making room for them by selling lesser ones, and staying clear of the worst. Marks highlights that the raw materials for the process include a list of potential investments, estimates of their intrinsic value, a sense of how their prices compare with their intrinsic value, and an understanding of the risks involved in each.

Marks explains that the starting point for portfolio construction is unlikely to be an unbounded universe. The goal is not to find good assets but good buys. Bargains get that way when the price is low relative to value, and potential return is high relative to risk. Investors can find underpriced assets by looking for things that are little-known, fundamentally questionable, unseemly or scary, or deemed inappropriate for "respectable" portfolios.

SETH KLARMAN: Generally, the greater the stigma or revulsion, the better the bargain

• little known and not fully understood

• fundamentally questionable on the surface

• controversial, unseemly or scary

• deemed inappropriate for “respectable” portfolios

• unappreciated, unpopular and unloved

• trailing a record of poor returns

• recently the subject of disinvestment, not accumulation

In this chapter, Marks provides examples from his experience with convertible securities and high-yield bonds, which were unpopular due to their complexity or poor ratings, but proved to be profitable for those who recognized their potential. He explains that bargains can be found in assets that are no longer popular, such as bonds, which had a decline in popularity as equities gained favor. Overpriced assets do not provide any benefits, while underpriced assets provide opportunities for bargains.

Overall, Marks stresses that investors must be willing to go against the herd mentality and search for underpriced assets to build a successful portfolio

The chapter discusses the importance of patient opportunism in investing. Waiting for bargains is often the best strategy, as it allows for discernment and inactivity. It's better to wait for investments to come to you than to chase them down. It's essential to recognize the condition of the market and invest accordingly. Buffett's philosophy on this is baseball-related, while Greenblatt's is based on early Japanese culture, which values mujo, meaning recognition of the inevitability of change. The chapter concludes that investing is the greatest business.

SETH KLARMAN: Still, calibration is important. Set the bar too high and you might remain out of the market for a very long time. Set it too low and you will be fully invested almost immediately; it will be as though you had no standards at all. Experience and versatile thinking are the keys to such calibration.

The article discusses the challenges of investing in a market where prospective returns are low and risks are high. Investors who pursue high returns in low-return environments often fail, and the pursuit of profit can lead to mistakes. One way to cope with this is to invest anyway, trying for acceptable relative returns under the circumstances, even if they're not attractive in the absolute. However, there is no easy answer for investors faced with skimpy prospective returns and risk premiums, and reaching for return may be exactly the wrong time to add to risk in pursuit of more return. Instead, investors should take risks when others are fleeing from it, not when they're competing with you to do so.

JOEL GREENBLATT: High valuations can often go higher and last for longer than expected, continually frustrating disciplined and patient value investors.

High valuations are extremely frustrating to the disciplined and patient value investors. It is essential to avoid being a forced seller, which means having no choice but to sell an asset regardless of price. The passage provides an example of a forced seller during the fourth quarter of 2008 when chaos hit the leveraged investment entities’ holdings of senior bank loans. Finally, the passage explains the consequences of the credit market contraction that affected large numbers of holders and how prices fell far below intrinsic value.

JOEL GREENBLATT: This is one of the hardest things to master for professional investors: coming in each day for work and doing nothing.

Knowing what you don’t know

Howard Marks emphasizes the significance of being a patient opportunist in investing, which means waiting for bargains to come to you instead of chasing them down. Investing is the greatest business, and it's important to recognize the condition of the market and invest accordingly. Two prominent investors who embody this philosophy are Buffett, whose approach is baseball-related, and Greenblatt, who bases his on the Japanese culture of mujo, meaning recognition of the inevitability of change.

HOWARD MARKS: Understanding uncertainty: Risk and uncertainty aren’t the same as loss, but they create the potential for loss when things go wrong. Some of the biggest losses occur when overconfidence regarding predictive ability causes investors to underestimate the range of possibilities, the difficulty of predicting which one will materialize, and the consequences of a surprise.

Investing in a market where prospective returns are low and risks are high can be challenging. Investors who pursue high returns in low-return environments often fail, and the pursuit of profit can lead to mistakes. Instead of reaching for return in these situations, investors should try for acceptable relative returns under the circumstances, even if they're not attractive in the absolute.

High valuations can frustrate disciplined and patient value investors, and it's essential to avoid being a forced seller. This means not being in a position where you have no choice but to sell an asset regardless of its price. The consequences of being a forced seller can be disastrous, as evidenced by the chaos that hit leveraged investment entities' holdings of senior bank loans during the fourth quarter of 2008. Additionally, the credit market contraction affected large numbers of holders, causing prices to fall far below intrinsic value. Therefore, it's crucial to wait patiently for the right opportunities to present themselves, even if it means being inactive for extended periods.

Key Takeaways:

Waiting for bargains is often the best strategy in investing

It's better to wait for investments to come to you than to chase them down

Recognizing the condition of the market is essential for investing accordingly

Buffett and Greenblatt have different philosophies on patient opportunism

The pursuit of profit can lead to mistakes in investing

Investors should take risks when others are fleeing from it, not when they're competing with you to do so

High valuations can frustrate disciplined and patient value investors

Avoid being a forced seller, which means having no choice but to sell an asset regardless of price

The consequences of the credit market contraction affected large numbers of holders and caused prices to fall far below intrinsic value.

Having a Sense for where we stand

In this chapter, Howard Marks discusses market cycles and how investors can navigate them. He argues that it is impossible to predict future market cycles with accuracy, but it is essential to understand where one stands in each cycle to make informed investment decisions. Marks stresses the importance of being alert to what is happening in the market and understanding the behavior of market participants. Some key takeaways from this chapter are:

Rather than predicting or ignoring market cycles, investors should try to understand where they stand in terms of each cycle and act accordingly.

Understanding present market conditions is critical to making informed investment decisions.

Buyers competing to put large amounts of capital to work in a market can lead to overheating and overvaluation.

Indicators of an overheated market include the issuance of high-yield bonds, debt raised for dividends, issuance of debt with coupons that could be paid with more debt, and buyouts in highly cyclical industries.

Investors should be alert to silver bullet or can't-lose investments, which can be a sign of an overheated market.

Investment decisions should be influenced by the current market environment, rather than solely based on future predictions.

The cyclical nature of markets emphasizes the importance of staying aware of surroundings when making investment decisions.

HOWARD MARKS: The riskiest things: When buyers compete to put large amounts of capital to work in a market, prices are bid up relative to value, prospective returns shrink, and risk rises. It’s only when buyers predominate relative to sellers that you can have highly overpriced assets. The warning signs shouldn’t be hard to spot.

Marks also suggests an exercise to assess the current state of the market and adjust investment strategies accordingly. Several experts praise this idea and suggest keeping a record of market swings for future reference. By being aware of the market cycles, investors can avoid potential pitfalls and make more successful investment decisions

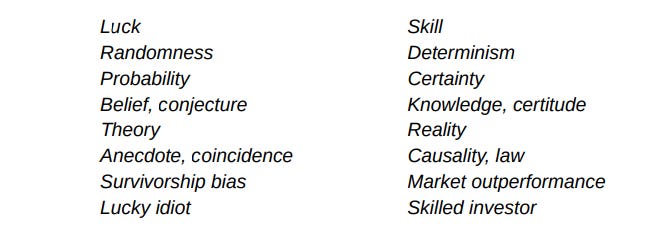

Investing is unpredictable and subject to randomness, luck, and chance. It is crucial to recognize that investment outcomes can come from both skill and luck. Investors must appreciate the role of luck in the investment world and acknowledge that good decisions can fail to work, and bad decisions can succeed.

HOWARD MARKS: Fear of looking wrong: It’s counterintuitive but extremely important: given the randomness and variability at work in our environment, it’s often true that good decisions fail to work and bad decisions succeed. In particular, investors are “right for the wrong reason” (and vice versa) all the time. You mustn’t let this frustrate you and convince you your good decisions were mistakes (unless so many prove wrong that you have to consider that possibility)

JOEL GREENBLATT: For good investors, as the time horizon expands, which allows skill to come into play, the probability distribution of long-term returns should narrow.

Key takeaways include:

Investors often receive credit they don't deserve due to randomness, and it's essential to have a large number of observations before judging a manager's ability.

The concept of "alternative histories" is discussed, and the past is challenged as being known and fixed. The quality of a decision is determined by the circumstances as they appeared at the time.

The article stresses the importance of understanding uncertainty in investing and avoiding the pitfalls of relying on short-term returns as an indicator of skill.

Defensive investing and avoiding herd behavior are emphasized, and long-term investing should narrow the probability distribution of returns.

Warren Buffet's appendix to "The Intelligent Investor" emphasizes that luck plays a significant role in investment success.

Investors must be stoic when good decisions don't lead to profits in the short run.

Overall, the chapter highlights the importance of recognizing the role of luck and uncertainty in investing and the need for a long-term and defensive investment approach.

HOWARD MARKS: Understanding uncertainty: People who think the future is knowable (and that they can know it) belong to what I call the “I know” school. They ignore the presence of uncertainty and act in ways that will increase profits if they’re right but expose them to increased losses if they’re wrong. Recognizing this, it’s important for all investors to figure out whether they know and act accordingly

Investing Defensively

Investing is not only about pursuing above-average gains, but it's also about avoiding losses. The author uses the metaphor of sports to explain the importance of defense in investing. The defensive investor's main focus is on not doing the wrong thing, which is achieved by conducting extensive due diligence, setting high standards, demanding a low price and generous margin for error, and diversifying one's portfolio. The avoidance of poor years and market crashes also plays a crucial role in investment defense.

JOEL GREENBLATT: Here is part of the tradeoff with diversification. You must be diversified enough to survive bad times or bad luck so that skill and good process can have the chance to pay off over the long term.

HOWARD MARKS: Understanding uncertainty: Despite the presence of uncertainty, many investors try to select the ideal strategy through which to maximize return. But if instead we acknowledge the existence of uncertainty, we should insist on building in a generous margin of safety. That’s what keeps your result tolerable when undesirable outcomes materialize

Key Takeaways:

Investing requires both offense and defense

Defensive investing involves avoiding losers

Defensive investors focus on not doing the wrong thing

A generous margin for error is critical in defensive investing

A balance between offense and defense is essential for long-term success

Risk control is crucial in investing

Joel Greenblatt, Christopher Davis, and Paul Johnson agree that finding a balance between offense and defense is crucial. While taking on some risk for higher returns is important, investors should be intelligent in their decisions and prioritize risk control.

The author emphasizes that a balanced approach is the best strategy for investing, as it emphasizes both risk control and the pursuit of returns. Ultimately, the choice between offense and defense is a challenging one, and investors must strike a balance between the two to achieve long-term success.

Avoiding Pitfalls

The chapter focuses on the importance of avoiding pitfalls in investment. The author emphasizes that avoiding losses is more important than striving for great investment successes. Pitfalls that lead to losses are categorized as analytical/intellectual and psychological/emotional errors. The chapter highlights the significance of being aware of the many pitfalls that exist and learning what they look like to avoid them. The author stresses the need to consider the full range of possible outcomes and avoid the "failure of imagination," which is not fully understanding the consequences of extreme occurrences. Additionally, the chapter discusses the danger of extrapolating the past into the future, which can lead to significant losses.

PAUL JOHNSON: The key to this wisdom is the phrase “you must allow for outliers.” Marks is unequivocal in his message.

JOEL GREENBLATT: The market eventually gets it right. In the short term, psychology and technical factors can make the wait for the long term exceptionally painful, but often this is the source of great opportunity.

Key takeaways:

Avoiding losses is more important than striving for great investment successes.

Pitfalls that lead to losses are categorized as analytical/intellectual and psychological/emotional errors.

It is essential to be aware of the many pitfalls that exist and learn what they look like to avoid them.

Consider the full range of possible outcomes and avoid the "failure of imagination."

Extrapolating the past into the future can lead to significant losses.

PAUL JOHNSON: The bullet on the role of leverage needs extra emphasis. Too many investors fail to appreciate this wise nugget.

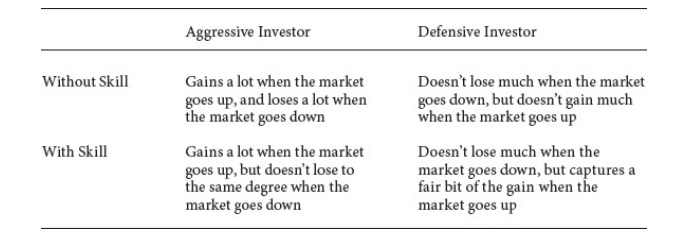

The chapter emphasizes the importance of alpha, or personal investment skill, in generating returns unrelated to the movement of the market. It contrasts passive investing with active investing, explaining that active investinAg attempts to outperform the market through buying and selling stocks or changing the portfolio's aggressiveness. However, unless active investors have superior insight, their risk-adjusted performance will converge with that of the index, and their portfolios should not be expected to perform better than a passive one.

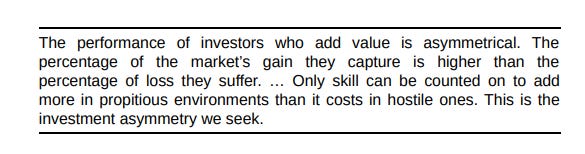

The chapter introduces beta as a measure of a portfolio's relative sensitivity to market movements and explains that a portfolio's increased return is explained by the increase in beta, or systematic risk, which is the risk that markets compensate for but not for risk other than systematic risk. Investors who lack skill simply earn the return of the market and the dictates of their style, while those who add value have asymmetrical performance, where the percentage of the market’s gain they capture is higher than the percentage of loss they suffer. Superior skill is the prerequisite for investment asymmetry.

JOEL GREENBLATT: However, unlike Oaktree, many investment firms raise a large amount of assets as a result of a good long-term record. With more capital, managers are often forced to invest differently than they did when they were building their great track record. Oaktree actually returns capital whenever the opportunity set shrinks. Few investment firms follow this path.

Key Takeaways:

Alpha, or personal investment skill, is essential to generating returns unrelated to market movement.

Active investing attempts to outperform the market, but without superior insight, risk-adjusted performance will converge with that of the index.

Beta is a measure of a portfolio's relative sensitivity to market movements.

Superior skill is the prerequisite for investment asymmetry, where the percentage of gain captured is higher than the percentage of loss suffered.

Asymmetry should be every investor's goal, and Oaktree returns capital whenever the opportunity set shrinks.

Reasonable Expectation

In this chapter, Howard Marks stresses the importance of setting realistic expectations for investment returns and being cautious about overly optimistic projections.

The key takeaways from this chapter are:

Investors should clarify their return goals, risk tolerance, and liquidity needs at the outset of an investment plan.

Reasonable return expectations are typically in the single digits or low double digits.

Achieving higher returns requires a combination of depressed buying conditions, exceptional investment skill, extensive risk bearing, heavy leverage, or good luck, but each of these has its limitations.

Investors should be skeptical of promises of high returns without risk and differentiate between reasonable and unreasonable expectations by asking themselves why they are being offered certain investment opportunities.

The Madoff scandal is cited as an example of accepting unreasonable expectations without question.

Unrealistic expectations played a role in the financial crisis and market crash, and investors should think about "good-enough returns" and avoid taking on risks that are not worth it.

Pulling it all together

I had a lot of fun reading this book again. This last paragraph will give you an overview of all the lessons we got to learn during this blog and book;

JOEL GREENBLATT: A good understanding of value and how to think about price movements is the key to successful investing. While there are many smart people who can master the estimation of value (especially if they are disciplined enough to stay within what Buffett calls their “circle of competence”), most investors fall short in the area of contextualizing market and individual security price movements. This is where the lessons from Marks’s book are so essential. So please feel free to read this chapter (and the entire book!) again and again—a true investment classic.

To achieve successful investing, one must have a solid understanding of an asset's value, including its tangible assets, cash generation ability, and growth potential. It's essential to have superior insight into value, learn things others don't, see things differently, and analyze better to achieve superior results. Buying below value is the most dependable route to profit and limiting risk, and investors must avoid being part of the herd.

Psychological and technical factors can dominate fundamentals in the short run, and the power of psychological influences, including greed, fear, and envy, must not be underestimated. Understanding market cycles and gauging market position from investor behavior is crucial.

Buying based on strong value, low price relative to value, and depressed general psychology is likely to provide the best results. Risk management is crucial, and investors should only bear the risk when the reward is more than adequate. Having a margin for error to render outcomes tolerable when the future doesn’t oblige is crucial. Defensive investing and margin for error give investors staying power and help them get through the low spots.

Key takeaways:

Understand an asset's value before investing

Buying below value is the most dependable route to profit and limiting risk

Avoid being part of the herd and psychological influences such as greed, fear, and envy

Understand market cycles and investor behavior

Risk management is crucial and only bear the risk when the reward is more than adequate

Have a margin for error to tolerate unforeseen outcomes

Defensive investing and margin for error give investors staying power

Focus on gaining a knowledge advantage regarding industries, companies, and securities

Avoid pitfalls, have reasonable expectations, and display real skill through asymmetrical performance for long-term success

Thanks for reading The Excellency Vault! Subscribe for free to receive new posts and support my work.

Thank you for this great article!

Howard Marks is "Hall of Fame" in everyone's book!