The Outsiders

The Outsiders

Eight Unconventional CEOs and Their Radically Rational Blueprint for Success

Today we will focus on ‘The outsiders: Eight Unconventional CEOs and Their Radically Rational Blueprint for Success’ which is a fascinating book that explores the unconventional leadership styles of eight CEOs who have achieved remarkable success in their respective industries.

The book highlights the strategies, principles, and philosophies that these CEOs have employed to build successful businesses and lead their teams to new heights. Each CEO profiled in the book has a unique approach to leadership, and their stories provide valuable insights and lessons for aspiring leaders and entrepreneurs.

The goal of this blog, will be for us to learn about what it takes to succeed in business and develop your own unique leadership style.

Main talking points

A Perpetual Motion Machine for Returns: Tom Murphy and Capital Cities Broadcasting

An Unconventional Conglomerateur: Henry Singleton and Teledyne

The Turnaround: Bill Anders and General Dynamics

Value Creation in a Fast-Moving Stream: John Malone and TCI

The Widow Takes the Helm: Katharine Graham and The Washington Post Company

A Public LBO: Bill Stiritz and Ralston Purina

Optimizing the Family Firm: Dick Smith and General Cinema

The Investor as CEO: Warren Buffett and Berkshire Hathaway

Radical Rationality: The Outsider’s Mind-Set

Similarities

The book profiles successful CEOs who ran companies in diverse industries and markets, without relying on retail concepts or intellectual property advantages. They had a shared set of principles that prioritized:

capital allocation

per-share value

cash flow

decentralized organizations

independent thinking

patience with acquisitions

‘These eight CEOs were not charismatic visionaries, nor were they drawn to grandiose strategic pronouncements. They were practical and agnostic in temperament, and they systematically tuned out the noise of conventional wisdom by fostering a certain simplicity of focus, a certain asperity in their cultures and their communications.’(p23)

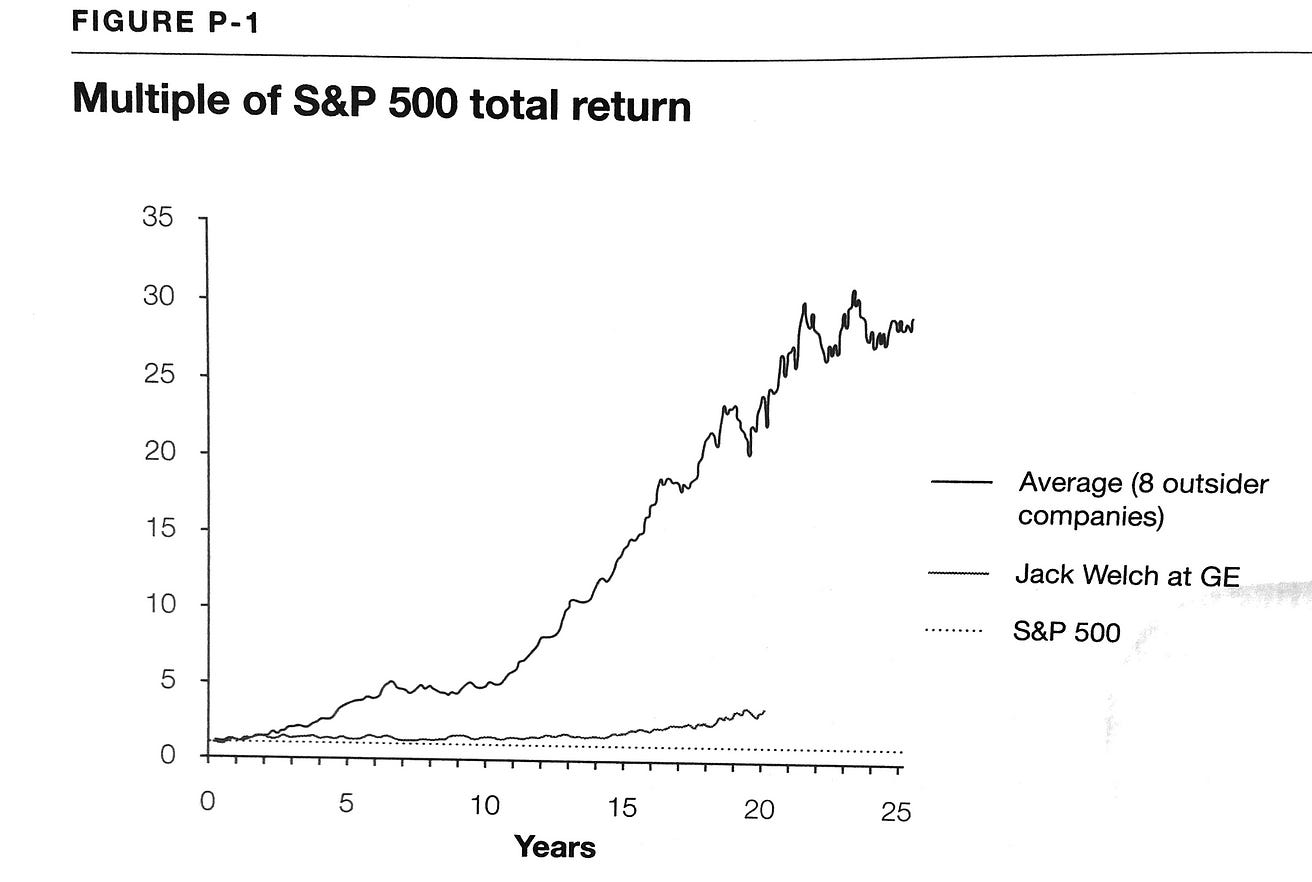

The CEOs were generally frugal, humble, analytical, and understated, and their operations were often located outside of the financial epicenter of the Boston/New York corridor. They were different from high-profile CEOs like Steve Jobs or Mark Zuckerberg, but they outperformed the S&P 500 and their peers by a significant margin.

Warren Buffett, in the 1986 Berkshire Hathaway annual report, reflected on his 25 years as CEO and identified a powerful force called the "institutional imperative." This force was comparable to teenage peer pressure and drove CEOs to imitate their peers' actions. Buffett warned that this force was nearly universal and that effective CEOs needed to find a way to ignore it. The best were able to avoid the noise and focus on what matters. After all, most companies do not outperform the benchmark.

These outsiders, despite independent thinking, shared similar management philosophy, including decentralization, large acquisitions, cash flow-based metrics, stock buybacks, and no dividends or Wall Street guidance.

These CEOs thought more like investors, with an emphasis on careful resource deployment and bold action when discrepancies between value and price were identified. This approach produced exceptional returns for shareholders over long tenures.

The lessons suggest a new, more nuanced conception of the chief executive's job with less emphasis on charismatic leadership and more on analytical skills and strategic decision-making, something we see confirmed by the book ‘Good to Great’ as well where the best focused on the business rather than how other thought about it or about the CEO'.

Crisis management: 1974–1982

What sets apart the great from the rest is their ability to trust themselves and their companies throughout good and bad times, they simply see the playing field and act upon it in a linear fashion. They always believe in a brighter future.

"Bad news is an investor's best friend. It lets you buy a slice of America's future at a marked-down price." -Warren Buffett

The period between 1974 to 1982 was marked by a combination of negative events such as an oil shock, fiscal and monetary policy disasters, and a political scandal that led to high inflation, two deep recessions, and bear markets.

However, outsider CEOs were active during this period, engaging in significant share repurchases or large acquisitions, while most managers sat on their hands. The outsider CEOs were "greedy," while their peers were "fearful," resulting in successful returns.

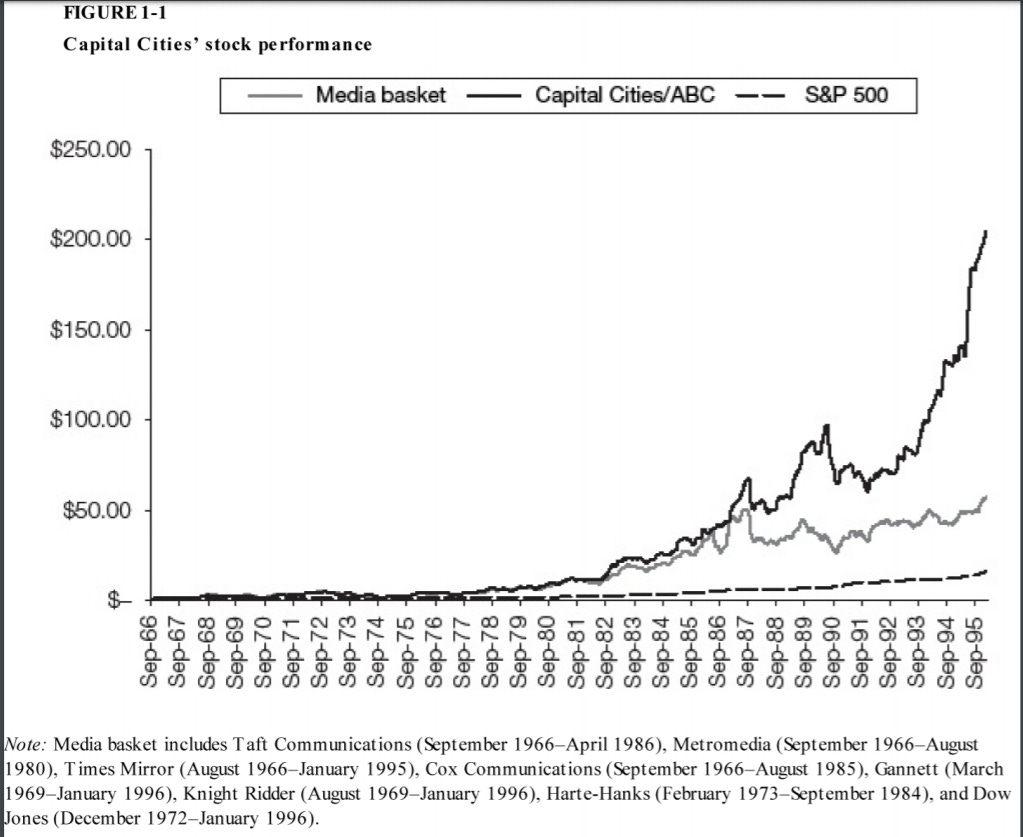

A Perpetual Motion Machine for Returns: Tom Murphy and Capital Cities Broadcasting

Tom Murphy at Capital Cities vs William Paley at CBS.

Paley's strategy was focused on making CBS larger through diversification and synergy, while Murphy's goal was to make Capital Cities more valuable by focusing on media businesses, selectively using leverage to buy occasional large properties, improving operations, paying down debt, and repeating.

Capital Cities under Murphy was successful because they moved slowly, developed real operational expertise, and focused on a small number of large acquisitions. They combined excellence in both operations and capital allocation, unlike other media companies that tended to diversify into unrelated businesses and overpay for marquee media properties.

The Timeline:

1966

After Smith’s death, Murphy became CEO.

1967

Murphy bought KTRK, the Houston ABC affiliate, for $22 million.

1968

Murphy bought Fairchild Communications, a leading publisher of trade magazines, for $42 million.

1970

Murphy acquired broadcaster Triangle Communications from Walter Annenberg for $120 million.

early 1970s

Murphy purchased several small dailies.

1974

He bought the Fort Worth Telegram for $75 million and the Kansas City Star for $95 million in 1977.

1980

He entered the nascent cable television business with the purchase of Cablecom for $139 million.

mid-1970s to early 1980s

Murphy became an aggressive purchaser of his own shares, eventually buying in close to 50 percent.

1986

Murphy bought the ABC Network and its related broadcasting assets for nearly $3.5 billion.

The acquisition stunned the media world and was greeted with the headline “Minnow Swallows Whale” in the Wall Street Journal. Buying out ABC was linked with Murphy’s conviction that he could improve the margins for ABC’s TV stations.

There are two basic types of resources that any CEO needs to allocate: financial and human.

The outsider CEOs in the book emphasize flat organizations and decentralized corporate staffs, recognizing that value is often created by local managers. Capital Cities is highlighted as a company where decentralization was central to its ethos, with extraordinary autonomy for operating managers being a hallmark of its culture.

This is a trait that was emphasized by ‘good to great’:

‘The good-to-great companies built a consistent system with clear constraints, but they also gave people freedom and responsibility within the framework of that system. They hired self-disciplined people who didn’t need to be managed, and then managed the system, not the people.’(p139)

Murphy believed that even the smallest operating decisions, particularly those relating to head count, could have unforeseen long-term costs and needed to be watched constantly. Expenses and capital expenditure were monitored through an extensive budgeting meeting each year.

Six daily newspapers, several magazine groups, and a stable of weekly shoppers were managed with only three people at headquarters.

Managers were expected to outperform their peers, and great attention was paid to margins, which Burke viewed as “a form of report card.” Outside of these meetings, managers were left alone and sometimes went months without hearing from corporate. The turnover was exceptionally low, by allowing people to strive the business felt like theirs, they cared!

The company's high margins were not achieved solely through cost-cutting, but also through investing in long-term growth. The CEOs recognized the importance of revenue growth and advertising market share and were willing to invest in their businesses to achieve leadership in local markets.

The main sources of capital for Capital Cities were internal operating cash flow and debt. The company consistently produced high levels of operating cash flow, which gave the CEO a reliable source of capital for acquisitions, buybacks, debt repayment, and other investments.

According to recent studies, somewhere around two-thirds of all acquisitions actually destroy value for shareholders.

The M&A value destruction was the central point of the book: The Value Killers: How Mergers and Acquisitions Cost Companies Billions—And How to Prevent It which you can find a quick summary about here.

Murphy and Burke relied on internal operating cash flow and debt for capital allocation. The company did not issue new stocks for twenty years except for selling stock to Berkshire Hathaway to finance the acquisition of ABC. Additionally, Capital Cities repurchased its shares repeatedly, causing a 47 percent reduction in total shares outstanding.

Acquisitions: Tying it together

The lack of unneeded workforce as well as the diligent budgeting led to the highest margins across the industry. This in itself allowed Capital City to acquire businesses at prices at attractive prices that would quickly increase in margins under their leadership. A sort of operating leverage unseen with competitors.

An Unconventional Conglomerateur: Henry Singleton and Teledyne

The steps

1960:

Singleton and Kozmetzky leave Litton and found Teledyne.

Teledyne acquires three small electronics companies and wins a large naval contract.

1961:

Teledyne becomes a public company.

Singleton acquires 130 companies between 1961 and 1969, mostly using Teledyne's high-priced stock.

1967

Singleton acquires Vasco Metals , making George Roberts president of Teledyne.

mid-1969

Singleton dismisses his acquisition team and stops acquiring, realizing that Teledyne's lower P/E ratio made its stock no longer attractive for acquisitions.

Singleton removes himself from operations and focuses on strategic and capital allocation issues.

mid-1970s

Singleton aggressively reallocated the assets in Teledyne's insurance portfolios, increasing the total equity allocation to 77% by 1981.

1984 to 1996

Singleton focused on management succession and optimizing shareholder value in the face of stagnating results at Teledyne's operating divisions.

1986

Argonaut, Teledyne's worker's compensation insurer, was the first spin-off in.

1987

Singleton declared the company's first dividend in 26 years as a public company, signaling a new phase in the company's history.

1990

Unitrin, Teledyne's largest insurance operation, was spun off , accounting for the majority of Teledyne's enterprise value at the time, and had excellent returns under its new leadership.

1991

Singleton retired as chairman to focus on cattle ranching operations but returned in 1996 to negotiate the merger of Teledyne's remaining manufacturing operations with Allegheny Industries and fend off a hostile takeover bid by Bennett LeBow.

Singleton delivered a remarkable 20.4 percent compound annual return to his shareholders (including spin-offs) from 1963 to 1990, leaving his peers and the market far behind.

The Formula

During the 1960s, conglomerates were a popular business model due to high stock prices and the lack of competition for acquisitions. However, Singleton, chose a different approach, focusing on profitable and growing companies with leading market positions, often in niche markets.

Instead of integration and synergy, Singleton and Roberts emphasized extreme decentralization, which generated remarkably consistent profitability and high returns on assets for Teledyne's operating businesses.

Singleton believed that repurchases were more tax-efficient than dividends for returning capital to shareholders, using them as a capital allocation benchmark and tendering for his shares when returns were attractive. He invested in companies with low P/E ratios and invested heavily in Teledyne's insurance operations, which generated eightfold growth in book value.

Although Teledyne's noninsurance operations slowed down in the late 1980s due to market conditions and fraud charges, Singleton still focused exclusively on getting the best possible price for Teledyne in negotiations, ignoring other peripheral issues.

The conventional wisdom was that repurchases signaled a lack of internal investment opportunity, and they were thus regarded by Wall Street as a sign of weakness. Singleton ignored this orthodoxy, and between 1972 and 1984, in eight separate tender offers, he bought back an astonishing 90 percent of Teledyne’s outstanding shares. As Munger says, “No one has ever bought in shares as aggressively.”

Henry Earl Singleton VS Warren Buffett

Warren Buffett and Singleton share several similarities in their approach to business and investment. Both of them considered themselves primarily as investors rather than managers, and focused on capital allocation rather than operations. They ran highly decentralized organizations with centralized investment decisions, investing mainly in industries they knew well and having concentrated portfolios of public securities.

Moreover, they had similar approaches to investor relations, not offering quarterly guidance to analysts or attending conferences, but providing informative annual reports with detailed business unit information. They also did not pay dividends, with Teledyne not paying dividends for its first twenty-six years, and Berkshire Hathaway never paying dividends.

Both Singleton and Buffett had significant ownership stakes in their companies, thinking like owners because they were owners. They recognized the potential to invest insurance company "float" to create shareholder value, with insurance being the largest and most important business for both companies.

Lastly, both intentionally ran highly unusual "restaurants"(Phil Fisher analogy) that over time attracted like-minded, long-term-oriented customer/shareholders. Overall, their investment philosophies and approaches to business had several similarities, making them two of the most successful investors and CEOs of their time.

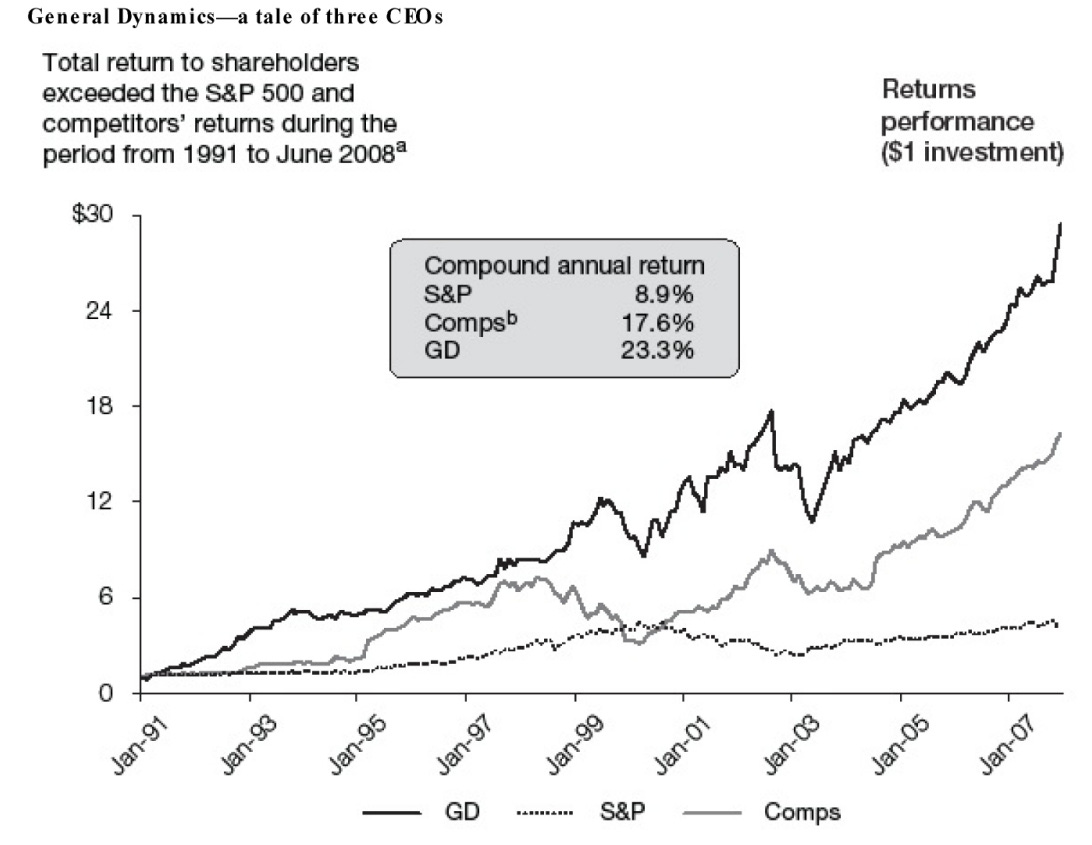

The Turnaround: Anders and General Dynamics

The steps

1989:

Fall of the Berlin Wall led to the collapse of the US defense industry's longtime business model based on selling large weapons systems.

Within six months of the Wall's demise, an index of the leading publicly traded defense companies had fallen 40 percent.

1985-1988:

General Dynamics overleveraged and had negative cash flow when Anders and Mellor implemented their plan.

Generated $5 billion of cash through tightening operations and selling non-core businesses deemed non-essential by Anders’s strategic framework.

Found overinvestment in inventory, capital equipment, and R&D, and wrung the excess out of the system.

Reduced overall headcount by 60% and corporate staff by 80%.

Relocated corporate headquarters from St. Louis to northern Virginia, instituted a formal capital approval process, and dramatically reduced investment in working capital.

Bid on projects only when returns were compelling, and the probability of winning was high.

Generated $2.5 billion of cash, and the company quickly became the leader among its peers in return on assets, a position it holds to this day.

Sold the majority of General Dynamics’ businesses, including its IT division, the Cessna aircraft business, and the missiles and electronics businesses.

Anders and Mellor brought a new focus on shareholders, which was a first in the defense industry.

1986:

General Dynamics brought in a new CEO, Stan Pace.

1987:

General Dynamics attempted to acquire Lockheed’s smaller fighter plane division but ended up selling the company’s dominant military aircraft business to Lockheed for $1.5 billion, a mind-bogglingly high price for the division.

Key point across the CEOs in this book:

As a group, they were, at their core, rational and pragmatic, agnostic and clear-eyed. They did not have ideology. When offered the right price, Anders might not have sold his mother, but he didn’t hesitate to sell his favorite business unit.

1990:

General Dynamics learned of the potential cancellation of its largest new aircraft program, the A-12.

1991:

Anders assumed the helm at General Dynamics, at the depth of the early 1990s, post–Gulf War bear market.

Anders adopted a long-term approach, focused on culture, capital investment, and organizational structure, instead of just short-term cash needs.

1993:

Anders retired from General Dynamics.

1997:

Mellor retired from General Dynamics.

Nicholas Chabraja succeeded Mellor as the CEO of General Dynamics.

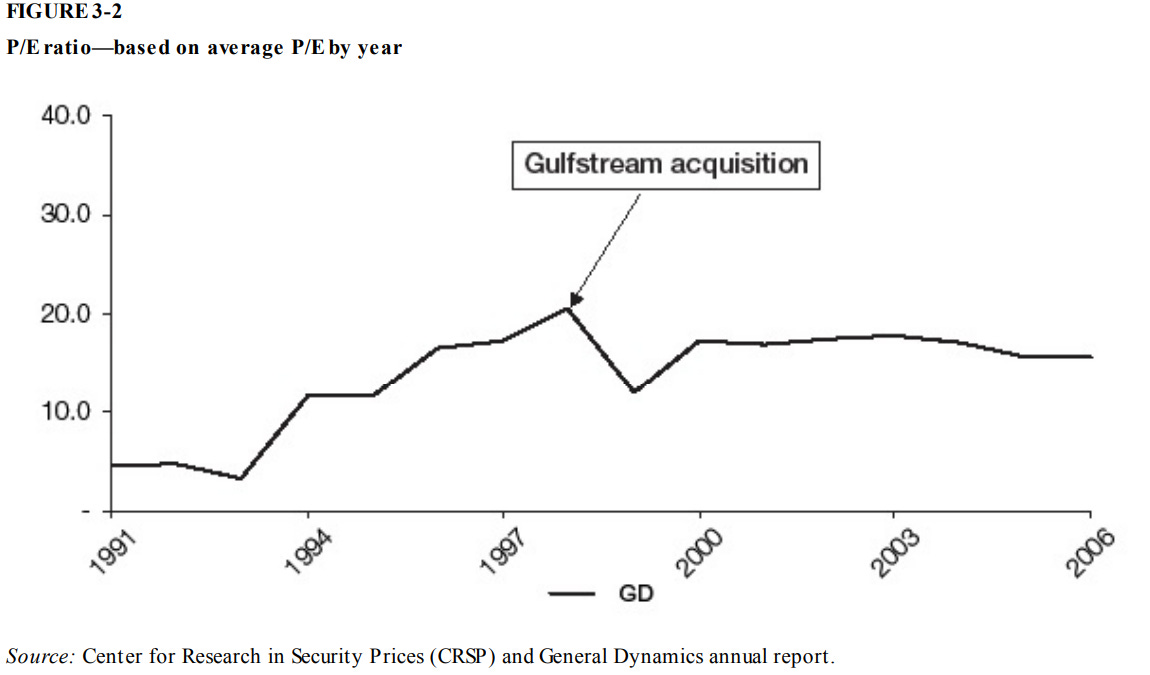

1999:

General Dynamics acquired Gulfstream in a bet-the-company transaction and represented 56% of General Dynamics' enterprise value.

The result

Chabraja’s Ethos

Nothing embodies Chabraja’s thinking more like the action he took by selling a large amount of General Dynamics stock to pay for the Gulfstream acquisition when the stock was trading at a significant premium to the historic norm. This move was opportunistic and helped the company grow and diversify while adding significant economic value for its shareholders.

This dilution was actually using an overpriced stock to buy an underappreciated asset and create long term value.

“Nick sold shares equaling one-third of the company to acquire a business that provided half of our consolidated operating cash flow.”(p76)

What made them great?

General Dynamics' success can be attributed to its unique and effective capital allocation strategies, including divesting non-core businesses, growing largest business units through acquisition, introducing key metrics such as cash return on capital, and making small acquisitions around existing business lines.

The company also focused on shareholders, tightened operations, reduced costs, and pursued practical, opportunistic, and flexible capital allocation. The CEOs pursued idiosyncratic allocation strategies and emphasized performance-based compensation, which aligned managers with shareholders.

They were not concerned with courting analysts, which allowed them to focus on their strategies and deliver strong shareholder returns. General Dynamics' approach was so successful that it was later emulated by Northrop Grumman.

Additionally, the company pursued a differentiated approach to raising and allocating capital.

Finally, the company pursued effective allocation of human and capital resources by decentralizing the organization and emphasizing performance-based compensation.

Value Creation in a Fast-Moving Stream: John Malone and TCI

The Timeline

1970:

John Malone joins General Instrument's Jerrold division, which is rapidly growing in the cable television equipment industry.

1972:

Malone is courted by Steve Ross of Warner Communications and Bob Magness of Tele-Communications Inc (TCI). Despite a lower salary, Malone chooses TCI because of larger equity opportunities and his wife's preference for Denver.

1973:

John Malone takes the helm at TCI, the fourth-largest cable company in the US, with 600,000 subscribers and debt equal to 17 times revenues. TCI has already been growing aggressively and using leverage to shelter cash flows from taxes.

1970s:

The cable television industry exhibits rapid growth, with subscriber counts growing over twentyfold, as rural communities across the country seek better reception of television signals for their favorite channels and programs. Cable television customers pay monthly and rarely disconnect, making the business highly predictable and quantifiable.

Pre-1977:

TCI has a frugal business model, with sparse headquarters and a rigorous budgeting process to maximize profits. Margins are the highest in the industry, and the company gains a reputation for under promising and overdelivering.

Managers in the field had a high degree of autonomy, as long as they hit their numbers. System managers who missed monthly budgets were frequently visited by the itinerant COO, and underperformers were quickly weeded out.

1977:

TCI stabilizes its balance sheet and is able to entice a consortium of insurance companies to replace the banks with lower-cost debt. This allows TCI to implement its strategy for maximizing financial leverage and leverage with suppliers, particularly programmers, by pursuing size as the key to creating value in the cable television business.

1978:

Malone and Magness created a supervoting class of B shares and were able to secure "hard control" of TCI.

1979:

Malone began an acquisition program, and TCI reached 2.5 million subscribers.

1980s:

TCI aggressively pursues scale through acquisitions, using financial leverage to buy more systems and lower programming costs per subscriber, thereby increasing cash flow.

1980s-90s:

Malone diversifies TCI's holdings, investing in technology, telecommunications, and international cable. He forms Liberty Media as a holding company for these investments.

1982:

TCI refrains from franchise wars and focused on acquiring less expensive rural and suburban subscribers.

1987:

TCI was twice the size of its next-largest competitor, Time Inc.'s ATC. Malone led a consortium of cable companies in the bailout of Ted Turner's Turner Broadcasting System.

Early 1990s:

HLT legislation limited the industry's access to debt capital, and the FCC tightened cable regulations.

1995:

Sparkman retires, and Malone delegates authority for the company's cable operations to a new management team led by Brendan Clouston.

Late 1990s:

Malone continued to selectively acquire large cable systems and launch new programming networks, including Starz/Encore and a series of regional sports networks in partnership with Rupert Murdoch and Fox.

1996:

TCI began centralizing customer service and spend aggressively to upgrade its aging cable facilities.

TCI badly missed its forecast, losing subscribers for the first time in its history and showing a decline in quarterly cash flow.

Malone takes direct management control of operations and quickly reduces employee headcount by 2500, halting all orders for capital equipment, and aggressively renegotiating programming contracts.

1997:

Teleport was sold to AT&T for $11 billion, a twenty-eight-fold return on investment.

1998:

Malone shifted his attention to finding a home for TCI.

The Sprint/PCS joint venture was sold to Sprint Corporation for $9 billion in Sprint stock.

TCI sells General Instrument to Motorola for $11 billion.

TCI is sold to AT&T.

The result

The compound return to TCI's shareholders was 30.3 percent, compared with 20.4 percent for other publicly traded cable companies and 14.3 percent for the S&P 500 over the same period.

What made Malone great

During John Malone's tenure at TCI, the company's success in the cable television industry was attributed to several key aspects. One of these was Malone's unique approach to capital allocation and tax minimization. Malone pioneered the use of debt in the cable industry, maintaining a ratio of five times debt to EBITDA, which helped shelter TCI's cash flow from taxes through the deductibility of interest payments. He was also parsimonious with equity and carefully managed the company's supply of net operating losses (NOLs) to avoid paying taxes.

Malone's value buying approach became the cornerstone of TCI's acquisition program, where companies were only purchased if the price translated into a maximum multiple of five times cash flow after the easily quantifiable benefits from programming discounts and overhead elimination had been realized. Cost efficiency was also a key factor, as Malone and his team trained their operations teams to be highly efficient in eliminating unnecessary costs from new acquisitions. This allowed them to reduce payroll, close studios, and move headquarters to a tire warehouse, all of which led to significant cash flow generation.

Malone's opportunistic buying approach allowed him to walk away from transactions that did not meet his rule, and he was also an opportunistic buyer of his own stock during periodic market downturns. TCI repurchased over 40% of its shares during Malone's tenure. Malone also added a sixth option to the standard menu of five capital allocation alternatives: investment in joint ventures. He leveraged the company's scale into equity interests in programmers and other cable companies, and these interests added significant value for shareholders with very little incremental investment.

In addition to these financial strategies, Malone provided a powerful mix of incentive and autonomy, which fostered a strong culture and employee loyalty at TCI.

Malone introduced a new financial and operating discipline to the company, telling his managers that if they could grow subscribers by 10 percent per year while maintaining margins, he would ensure that they stayed independent.

The company had an aggressive employee stock purchase program, and its operations were remarkably decentralized. TCI's culture was described as a group of frugal, action-oriented "cowboys" who defined themselves in counterpoint to the more conservative and bureaucratic Easterners who ran the other large cable companies.

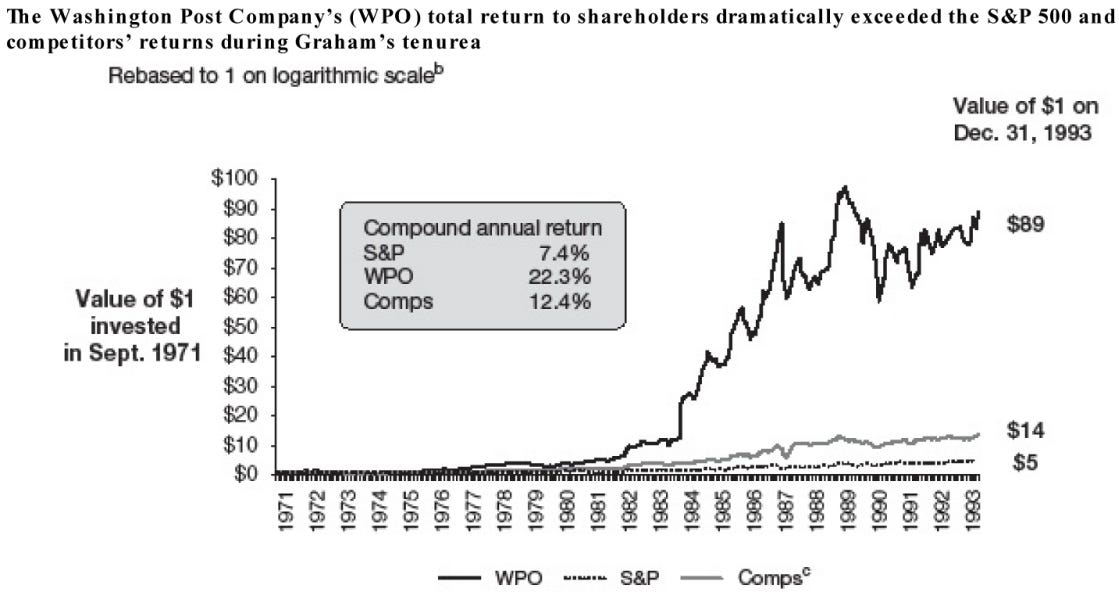

The Widow Takes the Helm: Katharine Graham and The Washington Post Company

The Timeline

1940

Katharine Graham marries Philip Graham, who would eventually become the head of The Washington Post Company.

1946

Eugene Meyer, owner of The Washington Post Company, taps Philip Graham to run the company.

1963

Philip Graham dies by suicide, and Katharine Graham becomes CEO of The Washington Post Company.

1967

Graham replaces longtime Post editor in chief Russ Wiggins with Ben Bradlee.

1971

The Washington Post Company goes public, raising $16 million, and becomes embroiled in the Pentagon Papers crisis. Graham decides to print the controversial report, securing the Post's editorial reputation and ensuring the success of the stock offering.

1972

The Washington Post begins investigating Republican campaign improprieties, which would eventually lead to the Watergate scandal.

1974

The Watergate scandal leads to Richard Nixon's resignation and secures a Pulitzer for The Washington Post.

1981

The Washington Star ceases publication, leaving the Post as the monopoly daily newspaper in the nation's capital and resulting in a dramatic increase in circulation and profitability.

Graham found a strong chief operating officer in Dick Simmons, who arrived in 1981 and rationalized the company's operating units, bringing in new executive talent and emphasizing strong performance relative to peers. Within several years, the company's newspaper and television margins had almost doubled, resulting in a surge in profitability.

1983

The Washington Post Company diversifies into new businesses, including cellular telephone franchises in six metropolitan markets.

1984

The company acquires the Stanley Kaplan test preparation business.

Alone among major newspaper company executives, Graham refrained from making large acquisitions during the high-water mark of deal making in the newspaper industry in the 1980s. Instead, she made two small acquisitions and diversified into new businesses.

1986

The Washington Post Company acquires Capital Cities' cable television assets for $350 million.

1988

The company sells its telephone assets for $197 million, realizing an extraordinary return on its investment.

1991

Graham's son Donald becomes CEO of The Washington Post Company.

1993

Katharine Graham steps down as chairman of The Washington Post Company.

Coached by Buffett, Graham aggressively bought her own stock, repurchasing almost 40 percent of the company's shares at rock-bottom prices over several years.

1990s to early 00s

The company continued to outperform its peers for another fifteen years.

The Result

What made her better than the competition?

Katharine Graham is known for her effective capital allocation strategy. She maintained low levels of dividends and debt, high levels of stock repurchases, and a careful approach to capital expenditures. She also had a patient and diversified approach to acquisitions, subjecting all potential transactions to rigorous analysis with the help of Warren Buffett.

Under Graham's leadership, the Post Company generated consistently strong cash flow. She made several great decisions that led to the company's success, including pursuing a buyback program, identifying and attracting talent to her company and board, and making an uncharacteristic buying spree during the early 1990s recession.

Graham also had a bias towards decentralization and lean corporate staffing. She was demanding and not afraid to make personnel changes to tighten operations and improve margins. She gave responsibility to promising managers at young ages and provided them with great autonomy. Despite occasional self-doubt, she made controversial and unconventional decisions that left a journalistic and financial legacy envied by her peers.

Donald Graham, Katharine Graham's son, continued to adhere to his mother's approach after becoming CEO. He led the Post Company to outperform its peers in the newspaper industry by making selected acquisitions, aggressively and opportunistically repurchasing stock, and keeping dividend levels relatively low

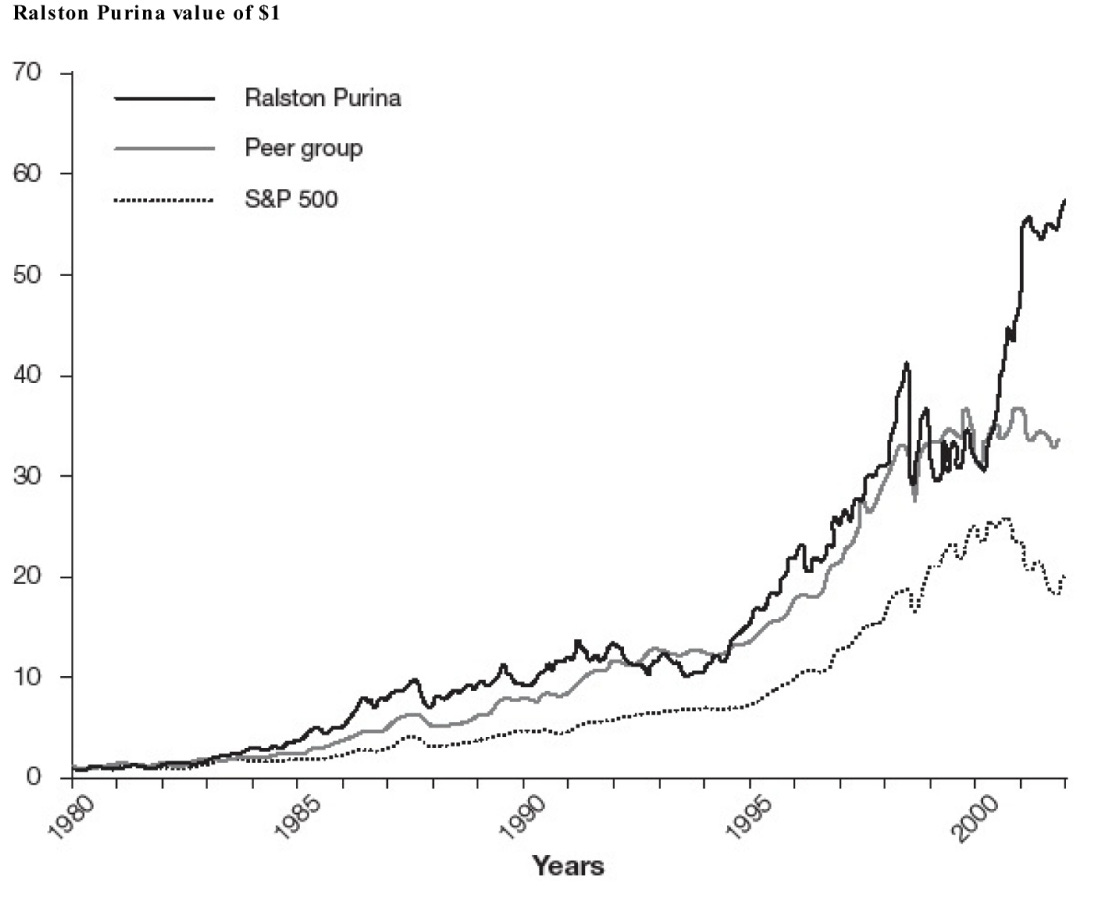

A Public LBO: Bill Stiritz and Ralston Purina

The Timeline

1980:

Hal Dean, CEO of Ralston Purina, announces his retirement. The company's stock price had not moved in a decade.

1981:

After conducting a thorough search for Dean's replacement, Bill Stiritz becomes the CEO of Ralston Purina, despite not being the lead internal candidate. He had spent 17 years at the company, working his way up from the grocery products division. Stiritz initiates an aggressive stock repurchase program.

1980s:

Ralston Purina, a Fortune 100 company with a long history in agricultural feed products, had engaged in a diversification program during the 1970s that left it with a melange of operating divisions, ranging from mushroom and soybean farms to the Jack in the Box chain of fast-food restaurants, the St. Louis Blues hockey team, and the Keystone ski resort in Colorado.

Mid-1980s:

Stiritz acquires Continental Baking, the maker of Twinkies and Wonder Bread, to Ralston’s stable of brands. Stiritz makes the largest purchase ever, acquiring the Energizer Battery division from Union Carbide for $1.5 billion.

Late 1980s:

Ralston’s percentage of revenues from consumer packaged goods rises to almost 90 percent. Pretax profit margins grow from 9 percent to 15 percent, and return on equity more than doubles, from 15 percent to 37 percent. Throughout the balance of the 1980s, Stiritz continues to optimize his portfolio of brands, making selected divestitures and add-on acquisitions.

1990s:

Stiritz aggressively restructures Ralston Purina, divesting of the company's non-core businesses and refocusing on pet food and cereal. He oversaw the introduction of Purina Puppy and Cat Chow, two of the most successful launches in the history of the pet food industry.

He continues to expand Ralston Purina's pet food business through acquisitions, including the purchase of Eveready Battery Company, which owned Energizer batteries.

Stiritz focuses on continued opportunistic stock buybacks, occasional acquisitions, and spin-offs to rationalize Ralston’s brand portfolio.

furthermore he begins the spin-off program with a collection of smaller brands, including Chex cereals and the ski resorts, into a new entity, Ralcorp.

Stiritz rationalizes and optimizes Ralston’s portfolio with the sale of the company’s remaining agricultural businesses, including the fast-growing protein technology business, for a record price to DuPont in a stock deal.

he spins off Energizer Holdings, the largest spin-off by far, leaving Ralston as a pure play pet food company, the dominant player by far in the US market.

2000s:

Ralcorp, originally a collection of neglected assets, grows to have an enterprise value of $5 billion.

The result

$1 turns into $60

How did he outperform?

William Stiritz's success as a CEO can be attributed to his unique combination of packaged goods marketing expertise and financial acumen. He saw capital allocation as similar to poker and used his skills to actively deploy leverage, prune less profitable businesses, acquire related businesses, and repurchase shares to achieve substantially higher returns on equity.

He believed in decentralization, reducing bureaucracy, and giving autonomy to managers, and used spinoffs as a way of furthering decentralization. Stiritz was an astute seller and had a proven ability to make high-value sales of assets while deferring capital gains taxes. He used cash for share repurchases and acquisitions, with a focus on buying businesses that could be improved by Ralston's marketing expertise and distribution clout.

Stiritz was a frugal buyer who avoided competitive auctions whenever possible and sourced acquisitions through direct contact with sellers. He valued analytical skill over charisma in a CEO and actively disdained the advice of outside advisers, negotiating their fees and using them surgically and sparingly. Stiritz guarded his time jealously, avoiding high-visibility philanthropic boards and time-consuming interactions with Wall Street. He was always open to new thinking and carved out blocks of time to focus on key business issues alone.

Overall, William Stiritz's approach to sales and divestitures involved selling noncore businesses that did not meet his criteria for profitability and returns, and he would sell any asset for the right price. He then redeployed the capital into higher-return packaged goods businesses, something we saw 2 CEOs ago. Stiritz's strategy of divesting noncore assets, repurchasing shares, and acquiring complementary businesses became industry orthodoxy, but he still surprised his competitors by selling Ralston to Nestlé for a record price. Stiritz's success as a CEO can be attributed to his unique combination of skills, temperament, approach to capital allocation and management

Optimizing the Family Firm: Dick Smith and General Cinema

The Timeline

1922

Phillip Smith, father of Dick Smith, opens his first movie theater in Boston’s North End.

1946

Dick Smith graduates from Harvard College with an engineering degree.

1956

Dick Smith becomes a full partner in the family business.

1961

Phillip Smith takes the company public, and Dick Smith becomes CEO of General Drive-In after his father’s sudden death.

1962

Dick Smith takes the helm of General Cinema.

1962-1970s

General Cinema expands its theater circuit into suburban shopping malls and develops two revolutionary new practices: lease financing and adding more screens per theater.

1968

General Cinema acquires American Beverage Company (ABC), the largest independent Pepsi bottler in the country.

1973

GCC acquires American Pepsi franchise.

1976

GCC partners with the largest orange grower's co-op to create Sunkist orange soda.

1977

GCC acquires Pepsi Cola Bottling Company and Washington, DC, franchise.

Late 1970s to early 1980s

GCC acquires several TV and radio stations, but fails to become a major player in broadcast industry.

1980

Hal Dean, CEO of Ralston Purina, announces his retirement. The company's stock price had not moved in a decade.

Early 1980s

Smith shifts focus to occasional, large opportunistic acquisition and a series of minority investments in public companies.

1981

After conducting a thorough search for Dean's replacement, Bill Stiritz becomes the CEO of Ralston Purina, despite not being the lead internal candidate. He had spent 17 years at the company, working his way up from the grocery products division. Stiritz initiates an aggressive stock repurchase program.

1984

GCC sells Sunkist to Canada Dry for $87 million, generating an exceptional return on investment.

Mid-1980s

General Cinema acquires Carter Hawley Hale, a retailing company.

Late 1980s

General Cinema divests its soft drink bottling business.

Early 1990s

General Cinema acquires Harcourt Brace Jovanovich, a publishing company.

1991

Peter Jovanovich replaces his father as CEO of HBJ.

General Cinema acquires HBJ for $1.56 billion, representing 62% of the company's enterprise value at the time. General Cinema spins off its mature theater business into a separate publicly traded entity, GCC.

Late 1990s

HBJ hires Smith Barney to conduct a sale process.

2003

General Cinema sells HBJ publishing assets to Reed Elsevier. General Cinema divests its interest in National Amusements, Inc., a theater chain.

2006

General Cinema sells its remaining theater assets to AMC Entertainment, Inc.

The Result

What made him outperform the rest of the pack

Dick Smith, CEO of General Cinema, managed the company collaboratively through the Office of the Chairman (OOC), a group of top executives that met weekly to encourage debate and decision-making. Smith delegated day-to-day operations to the OOC and division heads while focusing on strategic and capital allocation issues. He had a track record of giving executives responsibility early in their careers and offering competitive compensation through equity options and a generous stock purchase program.

The company's success was measured by cash earnings, which were consistently high, and debt-to-cash flow ratios were maintained at a minimum of three times. General Cinema made strategic use of debt to fund acquisitions of market leaders with solid growth prospects and respected brand names, ranging from 22 percent to 62 percent of the company's enterprise value at the time they were made. Smith was an exceptional seller of businesses when he saw dimming growth prospects and high valuations, selling three large divisions for record-setting prices.

Smith's approach to tax minimization was pioneering, keeping the company's effective average tax rate low. The company deployed cash into three primary outlets: acquisitions, stock repurchases, and capital expenditures. General Cinema was notable for holding large cash balances while waiting for attractive investment opportunities to emerge. Smith was a steady repurchaser of the company's stock over time, buying back one-third of the company's shares with a long-term internal rate of return on these buybacks of 16 percent. The company hit or exceeded every one of its targets, and the executive team felt like owners.

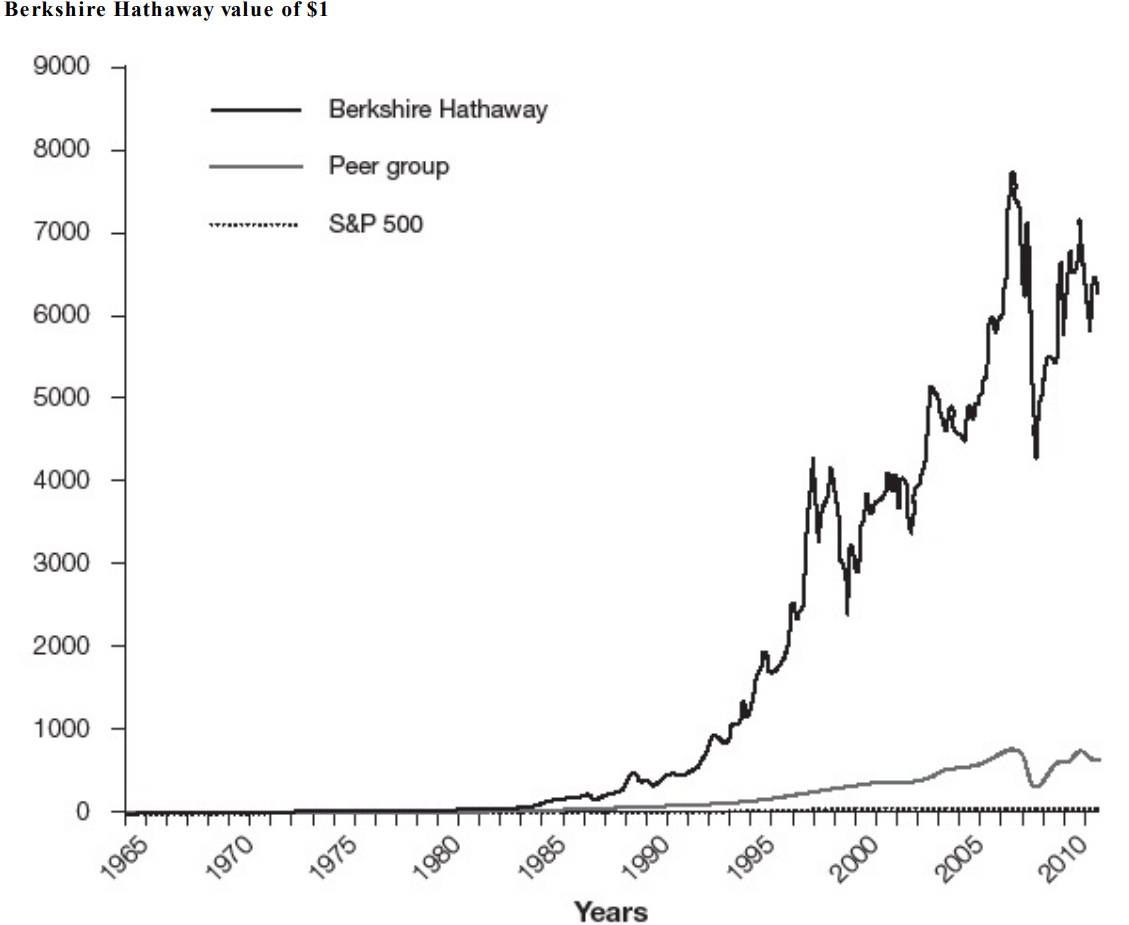

The Investor as CEO: Warren Buffett and Berkshire Hathaway

The Timeline

1930

Warren Buffett is born in Omaha, Nebraska.

1949

At age 19, Buffett reads The Intelligent Investor by Benjamin Graham, which becomes a turning point in his life and he begins following Graham’s value investing approach.

1952

Buffett graduates from Columbia and returns to Omaha, where he starts his career as a broker.

1954

Buffett gets a job offer from Graham to work at his investment firm, where he spends two years researching net/nets.

1956

Graham dissolves his firm, and Buffett raises a small investment partnership from friends and family.

1965

Buffett acquires Berkshire Hathaway, a New England textile company, after an extended proxy fight.

1970s

Buffett starts acquiring other companies and diversifying Berkshire Hathaway’s portfolio. Fear of inflation is a constant theme in Berkshire’s annual reports. Buffett and Munger believe that companies with low capital needs and the ability to raise prices are best positioned to resist inflation's effects. Berkshire's insurance portfolios increasingly include media and branded consumer products companies.

1972

Buffett and Munger buy See's Candies for $25 million, a pivotal investment in their shift from "cigar butts" to "franchises."

1980s

Buffett avoids the leveraged buyout craze that characterizes the era. Buffett focuses on adding to Berkshire's portfolio of wholly owned companies, including Nebraska Furniture Mart in 1983 and Scott Fetzer in 1985.

Late 1980s

Buffett makes investments in convertible preferred securities in Salomon Brothers, Gillette, US Airways, and Champion Industries.

1986

Buffett commits $500 million to help friend Tom Murphy acquire ABC, becoming the third of his "permanent" stock holdings alongside GEICO and The Washington Post Company.

1987

In advance of the October market crash, Buffett sells all of the stocks in his insurance company portfolios, except for his three core positions.

1989

Buffett invests an amount equal to one-quarter of Berkshire’s book value in Coca-Cola Company, purchasing 7 percent of its shares.

1990s

Berkshire Hathaway continues to grow and diversify its portfolio, becoming one of the largest companies in the world. Buffett becomes a philanthropist, pledging to donate most of his wealth to charity.

1991

Buffett is drafted as interim CEO of Salomon Brothers to help the company navigate a major financial scandal. He devotes himself full-time for a little over nine months to this project.

1999

See's Candies results are no longer reported separately.

Present day

Berkshire Hathaway's success is attributed to Buffett's shift in investment focus from "cigar butts" to "franchises," which has allowed for long-term pretax compounding of investment values. Berkshire Hathaway has a market capitalization of $140 billion and is one of the largest companies in the world. Buffett is widely regarded as one of the most successful investors of all time.

The Result

The Magic

Warren Buffett's exceptional success as a CEO can be attributed to his unique approach in three key areas: capital generation, capital allocation, and management of operations. Buffett's ability to generate low-cost funds for investment and invest them profitably has been a critical component of Berkshire Hathaway's long-term success. Berkshire's primary source of capital is float from its insurance subsidiaries, which has almost entirely eschewed debt and equity issuances. He has created a capital "flywheel" at Berkshire, with funds being used to acquire other cash-generating businesses whose earnings in turn fund other investments.

The insurance business, which emphasizes profitable underwriting and float generation over growth in premium revenue, is a critical foundation of Berkshire's extraordinary growth. National Indemnity, Berkshire's largest P&C insurer, saw a spiky pattern of revenue, which would be virtually impossible for an independent, publicly traded insurer to explain to Wall Street. However, Berkshire's insurance subsidiaries are shielded from Wall Street scrutiny because they are part of a larger diversified company, providing a significant competitive advantage.

Earnings from wholly owned companies have become increasingly important over the last two decades as Buffett has added aggressively to Berkshire's portfolio of businesses. In both insurance and investing, Buffett believes the key to long-term success is "temperament," a willingness to be "fearful when others are greedy and greedy when they are fearful."

Buffett insists on centralized capital allocation when he buys a company, focusing on investing in publicly traded stocks and acquiring private companies. He has never paid a dividend or repurchased significant amounts of stock. He concentrates on businesses with attractive returns on capital and gets out of low-return businesses. His approach to managing Berkshire's stock investments is characterized by a high degree of concentration and extremely long holding periods. Buffett believes exceptional returns come from concentrated portfolios, and the top five positions in Berkshire's portfolio have typically accounted for a remarkable 60-80% of total value.

Buffett's unique acquisition approach involves purchasing private companies through a system where owners of leading private companies call him. He arrives at deals with extraordinary speed, often within a few days of first contact, and never spends significant time on traditional due diligence. He delegates everything except capital allocation decisions and does not rely on intermediaries such as business development teams or investment committees for advice. He only buys companies in industries he knows well, allowing him to focus quickly on key operating metrics and wait for no-brainers.

The touchstone of the Berkshire system is extreme decentralization. Berkshire has no regular budget meetings, and CEOs of its subsidiary companies rarely hear from Buffett unless they call for advice or seek capital. Buffett spends most of his time on capital allocation and as little time as possible managing operations, where he feels he can add little value. He believes this extreme form of decentralization increases overall efficiency by reducing overhead and releasing entrepreneurial energy.

Buffett's unique approach to investor relations involves spending no time with analysts, never attending investment conferences, and never providing quarterly earnings guidance. Instead, he communicates with his investors through detailed annual reports and meetings, both of which are unique. He manages his schedule to avoid unnecessary distractions and preserves uninterrupted time to read and think. He prides himself on keeping a blank calendar, devoid of regular meetings, and does not have a computer in his office or a stock ticker.

Finally, Buffett's culture at Berkshire reinforces a powerful set of values that values frugality, independent thinking, and long-term stewardship. He has famously eschewed splitting Berkshire's A shares to self-select for long-term owners, instead creating a lower-priced class of B shares. In 2010, he agreed to split the B shares further 50:1 in connection with the Burlington Northern deal.

In summary, Warren Buffett's success can be attributed to his unique approach to investing, which emphasizes fundamental analysis, value investing, and a long-term perspective. He has also built a successful conglomerate in Berkshire Hathaway by acquiring well-run companies with strong management teams and allowing them to operate independently. Furthermore, Buffett's culture at Berkshire reinforces values such as frugality, independent thinking, and long-term stewardship, which have contributed to the company's success over the years.

Buffett's investment philosophy has inspired many investors around the world, and he is widely regarded as one of the greatest investors of all time. His annual shareholder letters, in particular, are considered a must-read for anyone interested in investing or business. As of 2021, Warren Buffett is still the chairman and CEO of Berkshire Hathaway, and his legacy continues to inspire generations of investors to come.

What makes the Greatest the best

The average company turned $1 into $600 or 600x the initial amount. In this following summary, I will explain what the best have in common and how they grow a business into behemoths.

The bottom line

Outsider CEOs are successful because they rely on their own sound facts and reasoning and develop succinct analytical templates that focus on key variables and empirical data.

The value of a dollar invested in outsider CEOs' companies was significantly higher than their peers, the broader market, and Jack Welch.

Successful outsider CEOs focus on maximizing value per share, managing financing, and complementing the numerator with the denominator.

They are master delegators who push operating decisions down to the lowest levels of their organizations, but do not delegate capital allocation decisions.

Successful outsider CEOs are independent and act with a minimum of input from outside advisers and are comfortable acting alone or with very little input.

They are patient and willing to wait long periods for the right opportunity to emerge, and they avoid overpriced "strategic" acquisitions and stay on the sidelines during acquisition feeding frenzies.

Successful outsider CEOs consistently apply a rational, analytical approach to decisions, and they are pragmatic and do not overanalyze or overmodel.

They have a long-term perspective and invest in their businesses to build long-term value, even if it means sacrificing short-term earnings.

Successful outsider CEOs tune out Wall Street analysts and focus on their customers and long-term competitive positions.

They are often contrarian and willing to zig when others zag, with a focus on optimizing within given circumstances.

Successful outsider CEOs emphasize frugality, patience, independence, occasional boldness, rationality, and logic.

Their success is based more on temperament than intellect.

The experiences and lessons of these CEOs are relevant to virtually any manager or business owner, regardless of their area of expertise or specialization.

This book, despite underwhelming 200 pages was concentrated with information. This is a book you want to read and reread as it contains 8 different CEOs/companies each with different stories.

Despite the different stories, every single CEO shares traits with the rest. The greatest indeed are so similar at the core that the lessons learned within this book apply to other CEOs laid out in other similar books.

If you liked this blog, please make sure to share it around and let me know what concrete steps you are taking to become top-tier yourself in the comments!

Thanks for reading TheShortBear’s Vault!

More Books:

"Good to Great: Why Some Companies Make the Leap and Others Don't"

by Jim Collins

→This book examines the characteristics of companies that have achieved sustained success over time and provides insights into how other companies can emulate their success.

"Built to Last: Successful Habits of Visionary Companies"

by Jim Collins and Jerry I. Porras

→This book examines the characteristics of successful, long-lasting companies and provides insights into what sets them apart from their competitors.

"The Lean Startup: How Today's Entrepreneurs Use Continuous Innovation to Create Radically Successful Businesses"

by Eric Ries

→ This book provides a framework for building successful startups by focusing on continuous innovation and customer feedback.

As an Aspiring Business Owner. Personally I will definitely have to work more on learning about "decentralized organizations". I also think it would be very interesting to learn generate ideas based on combining "decentralized organizations" + "First Who then what" from your previous post.