Misses following the 2021/22 bear market

Misses following the 2021/22 bear market

A compilation of the best opportunities I had prepared for and missed.

I have been trading for 11 years now.

After dawn, the active day and getting towards what I felt was the sunset of my active small cap trading career, I knew I had to change in order to evolve.

Trough my extensive documentation on twitter, you saw me shift my approach from an active approach to an increasingly passive one. In order to continue compounding I had to focus on the long term and slowly but surely I let go from my old identity to evolve. The book was not closed, but a new chapter started.

This blog will go through my investment misses. Despite the hindsight nature of the setups that ended up working according to the plan, each opportunity below was spotted before their big move and management would have led to a big expected value.

I will go through most examples I have documented over the past 3 years.

The misses

COSTCO Wholesale Corp. ($COST)

I came across Costco through my studies on Berkshire and more specifically Charlie Munger. The company is what would develop into a ‘Nick Sleep’ playbook opportunity, characterized by it’s ‘scale efficiencies shared’ business model.

Companies such as Costco or Amazon have similar models. By providing a better offering and scaling the business with a pure customer focused approach, the businesses increase their moat and become hard to derail.

I will refer to this blog will describe in detail why Nick sleep chose Costco (and Amazon) as his top investment. You saw me use this knowledge when I made Mercadolibre my top investment towards the 2022 lows.

The Setup

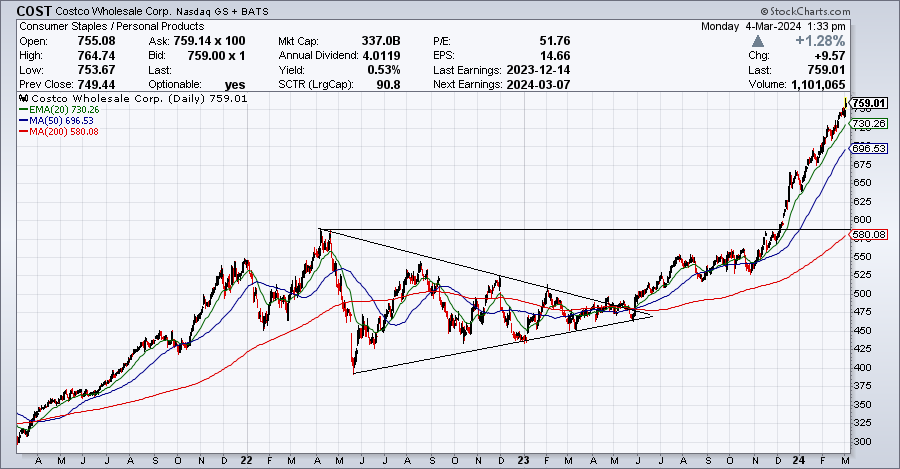

While many stocks panicked in 2020, Costco flagged and continued running almost 100% into the 2021/22 bear market. While most stocks were busy crashing, Costco started to consolidated for 1.5 years.

A wedge started forming and resolved higher as the market bottomed.

Buying the $500 wedge and whole number breakout would have provided you with a great risk reward profile and would have later allowed for pyramid to take place.

This was a chance to own one of the best assets in the world. I missed it as I was leveraged long other assets. The prospects of quicker gains within other assets led me to ignore, however a lesson ensued.

Compounding > Quick Gains.

When confronted with the prospect of a great entry on a compounder or a momentum trade, the missed potential of a compounder outweighs the somewhat better immediate trade expected value. The cost of a missed compounder incrementally increases as time goes on.

While a reentry at a later date is not erroneous, the risk reward profile and pyramiding potential is not gone and thus the risk profile is far worse.

Sequence: Wedge breakout → $500 breakout→ All time high breakout→20ema ride

Shopify ($SHOP)

Shopify had long been on my wishlist and was one of the first investment I bought as I transitioned from a strictly active trading approach to investing. The thesis at the time revolved around the E-commerce exposure and general growth of the business.

Even though I would like to think I knew much, part of the investment thesis was erroneous at the time as I did not yet possess the expertise I so dearly wanted.

Nonetheless I started buying SHOP in the 70s and started to average down. In August 2022 when we looked to breakout higher I added and subsequently had to endure yet a fail attempt to move higher. I sized down and ended up cutting the position into the breakdown, losing a good chunk of capital while doing so.

Shopify reclaimed and proceeded to breakout higher off of an inversed head and shoulders pattern. despite the choppiness we continued higher and doubled over the subsequent year.

The lesson I retained was to zoom out and remember the general investment. I was investing, yet managing the position as a trade. The balance between leaving an investment to compound and adding to pyramid is a frustrating one and one I consciously and consistently work on.

Gartner Group ($IT)

Gartner conducts research on technology and shares this research both through private consulting as well as executive programs and conferences. I became interested in the company when I understood that major banks and investors all used the data provided by Gartner to analyze companies.

Companies such as Bloomberg, Gartner, Moody’s and alike all profit from a secondary market. Rather an investment invests in an asset or not they have to do the research first and Gartner indirectly receives a fee each time they do so.

This creates a continuous stream of income and it shows within the metrics I saw.

20%+ ROCE

Massive ROE

68% gross margin, 19% operating margin, 15% net margin

Now that I saw the company as high grade I focused on a good risk reward in order to enter. We got it in mid 2022.

We gapped up through an earnings beat, breaking over the overall trendline. Following the breakout we consolidated, resting on the 200ema and continued building a bigger wedge, pressing against all time highs. The recent earnings beat led to a final breakout higher. IT 0.00%↑ is now looking to break higher after consolidating for the first quarter.

I missed it due to what I perceived to be a loose base after the initial gap higher. I found it hard to manage the trade given the yearly lows near $225 was $75 lower than the $300 price you had to pay to own it. The late 2023 entry was hard to commit to for me because of the failed breakout in July 2023.

Overall the stock almost got me in but I decided to stay away.

Once again the question remains the balance between owning a good asset and trading the setup. Reducing the size and widening the stops might be the correct approach the ‘better’ the compounding potential of the company. When the company could go 500% higher, it is risky in itself to be tied to closer stops because of the original size. The return comes through the RR, not the win rate.

The Sequence: Earnings gap up and trendline breakout → Secondary pennant breakout→ 200ema retest→350 half number and ath breakout→200ema retest→ EP breakout→(soon: wedge breakout at 470)

Monster Beverage Corp.($MSNT)

This ticker came across my desk due to its track record. Monster ranks within the best compounders ever. It’s stock went from $0.03 in 1994 to $55.02 in 2024, compounding at 16.3% over the past decade.

53% gross margin, 28 operating margin, 23$ net margin

28% ROIC, 23% ROCE

I liked the metrics I saw, however the price matched the quality of the company. I had to pay 9x sales and 40x earnings for a company growing at about 11% per year.

The price got me to avoid the ticker despite the setup. I was proven right at first after the ticker rested sideways for months and even broke back under support earlier this year. Despite the tricky action, the company has steadily grown earnings and is looking to break higher above $60, a good 20% above the $50 breakout area.

Sequence: 200ema test → 50$ breakout→52.5 breakout→ failed 200ema hold→ breakout retest→ 200ema hold→(soon:60 breakout)

Nvidia ($NVDA)

Obviously the biggest opportunity of the AI era and the biggest miss of all despite making money on the name. I was studying AI and using it right from the get go, and despite understanding NVDA’s position within the ecosystem, I did not jump onto the bandwagon when odds were best.

Latest when I saw Druckenmillers portfolio should I have reevaluated the opportunity. I knew bubbles of a secular nature take years to develop and I understood that NVDA was perfectly positioned to reap the benefits.

NVDA had developed and invested so much into AI chips that competitors were left without the ability to compete and through it directing the entire AI spending straight onto its balance sheets.

The perfect spot to enter was around the time we heard about Druckenmillers positon at the start of 2023. We knew the potential of AI, had time to research and the market provided us with great RR.

In Jan 2023, when the market put in the bear market lows, NVDA broke over its 200ema, breaking out of its down trending trendline in the process. Additionally this led to a higher higher, $200 whole number breakout and a multi-month horizontal consolidation breakout.

NVDA showed its cards right away as it trended with the somewhat aggresive 20ema. In June NVDAs positioning within AI got confirmed by its earnings and we got an all time highs breakout (EP setup). (I had my doubts into those earnings and actually lost 250k via puts, a bet I had put on via puts to minimize damage in case of such results).

NVDA then proceeded to rest after a staggering 100% move within a few months. After a failed breakdown attempt in November, NVDA built a pennant and horizontal breakout on the $500 whole number and broke out. At this point I was ready and entered heavily, selling into the high 500s, once again piking.

NVDA would continue the same uptrend as in H1 2023, riding the 20ema.

The main takeaway is to trust the leader within a secular bubble and trust the duration of such a bubble (1.5-2y minimum). Druckenmiller knew this and took advantage.

I have much more thoughts about this ticker and obviously given the 9fig potential this one will hurt forever and needs to be studied to the highest degree.

Sequence: 200ema reclaim→ $200 whole number breakout(also horizontal breakout), 20ema ride→ EP setup→ 200ema breakdown fake out→ $500 whole number horizontal breakout (+ wedge)→20ema ride

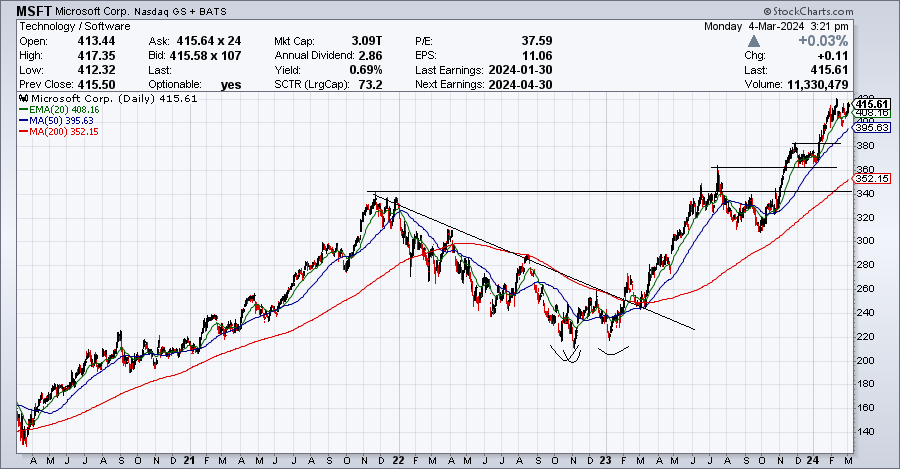

Microsoft ($MSFT)

Microsoft is in my view the second best AI play of 2023. While NVDA tapped into the core of AI through making itself the only possible option to build AI infrastructure, Microsoft was the best at implementing this new technology.

On top of its stellar earnings, Microsoft had managed to secure a stake in OpenAi, which is the company that started this entire AI secular change.

“OpenAI was founded in 2015 as a not-for-profit organisation, which now owns the for-profit subsidiaries created in 2019 to facilitate Microsoft’s investment. People familiar with the deal say Microsoft has in total committed up to $13bn to OpenAI, including a $10bn expansion announced in January this year

Reports before, and for months after, January’s announcement of what the two companies described as a “multiyear, multibillion-dollar investment” had suggested that Microsoft could end up with a 49 per cent stake..”

Microsoft not only did well on its own, but the exposure to AI and its ability to quickly integrate the new AI tech into existing products were a great combination for multiples to expand and earnings to grow.

I bought GOOGL instead because of there investing history into AI, a humongous amount of data through their search business and the incredible number of developers working for the company (27k). GOOGL not only was late(which is why multiples were low), but later on kept on messing up the execution of new or updated products. I ended up selling because of this failed execution and through the risk I see to GOOGL’s moat through new competition and AI generally. If I see their execution improve I might reenter at a later date.

Microsoft bottomed near the market lows and started to form a strong trend. Despite the overall strong trends, the stock provided a failed breakout before forming a cup and handle instead. More than the technical setup, Microsoft provided a leader to invest into the AI theme. NVDA and MSFT were both strongly linked to AI and gave time to join the trend, however some like me chose to ignore it.

The Sequence: 200ema reclaim→200ema retest→20ema ride until ath→ failed breakout→ cup and handle breakout→ continuation breakout→20ema ride

DraftKings ($DKNG)

Draftkings crashed after the 2021 top but steadily grew its revenue in the meantime.

We formed a clear double bottom and broke out of a cup and handle/double bottom formation. We then proceeded to slowly but surely recover. 100% within 1year.

Even though this is not my favorite long-term investment candidate, the setup was clear.

Sequence: Double bottom/cup and handle → 20ema ride→ double bottom

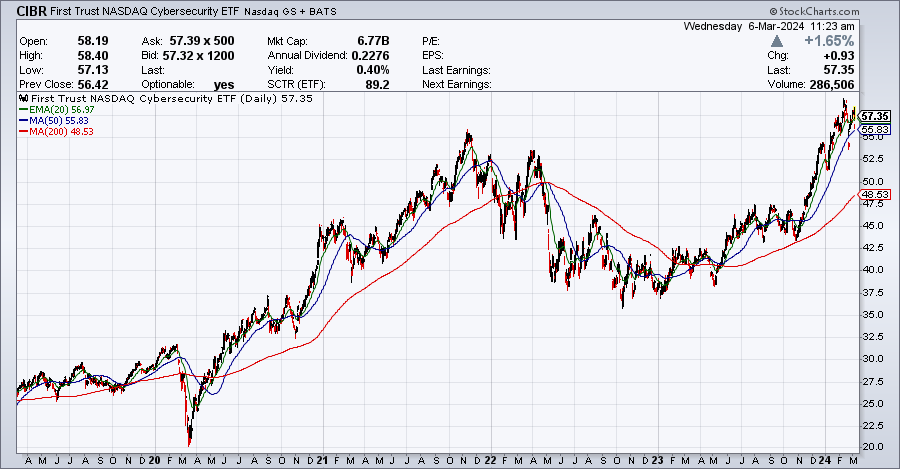

Cloudflare ($NET)

Cloudflare was known as one of the 2020 craze darlings. No multiples was high enough and this case the multiples rose from near single digits to 80x sales.

Once the bubble popped we had so much multiple normalizing to do that the stock crashed by -75%, however the company itself continue to perform and managed to grow their earnings from $500mil at the top of the bubble to $1.3b revenues now.

The combination of fast growth and of the stock itself led to a multiple compression.

Before the recent breakout NET was trading at a ~15x sales multiple.

While 15x sales is expensive by many standards, Cloudflare manages to keep high margins and high growth as its key attributes, making for a decent longer term position.

The cybersecurity space as a whole was a space I saw as the most likely to outperform out of the bear market.

CIBR, representing the cybersecurity ETF showed clear strength and as the space itself started to breakout in March 2023 and while Crowdstrike started its spectacular rise, cloudflare missed earnings and continued consolidating.

Instead, Cloudflare broke out after the October market correction.

At that point I was exiting CRWD and did not have the mental fortitude to long another cybersecurity stock while selling my main cybersecurity exposure.

Instead of protecting me, CRWD continued higher and I missed NET.

Sequence: December breakout→50ema ride→ 20ema ride

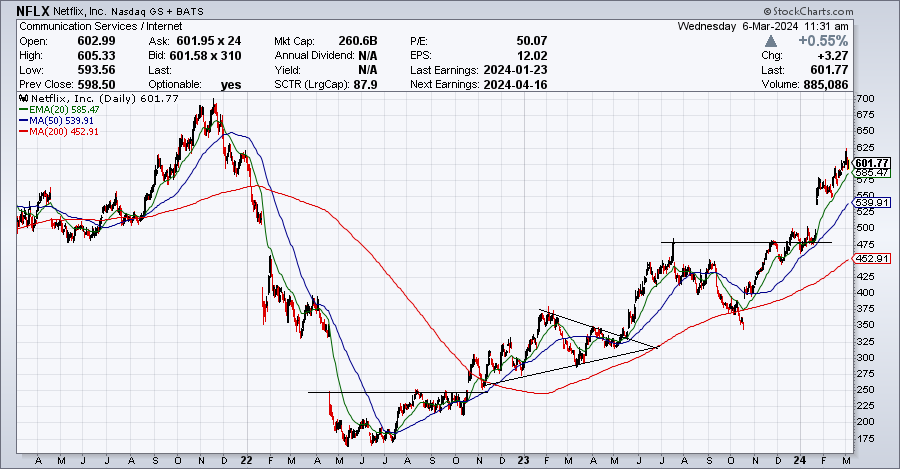

Netflix ($NFLX)

Netflix and META were the two mega caps that crashed the hardest during the 2022 bear market. Previously indestructible companies seem to have lost their way.

Towards the bottom, many super investors decided to sell their holdings such as Pershing squares Bill Ackman. The sentiment was at a low point.

Nonetheless NFLX looked interesting to me following the March to July bottoming process. Once we reached the neckline and consolidated, starting to push against it and create pressure I started to forge a trade plan.

I started buying a massive call position, equaling to about 500 contracts (50k shares) to start with the intention of holding and adding to it once on our way to the first target at the 350 gap fill.

I wanted NFLX to breakout higher before earnings given the risk of a gap down and the loss I would be facing should I be wrong. NFLX tried breaking out but failed and then proceeded to break under the 20 and 50ema before earnings and thus I cut the position.

The arbitrary nature of the bet in front of earnings led me to miss this massive rise, which mainly materialized through a multiple expansion.

I wanted this breakout so bad that I ended up micromanaging what could have been an easy starter for a long term hold, a reoccurring theme in my trading.

Precise and massive size VS nimble and bigger stops for the bigger move

We ended up moving higher in a choppy manner with a scare following the 200ema loss and subsequent reclaim. Overall the only way not to get shaken out is through a low average and simply leaving it alone, trusting in the company itself to continue performing.

Sequence: EP setup and breakout→ wedge breakout→200ema retest→ breakout

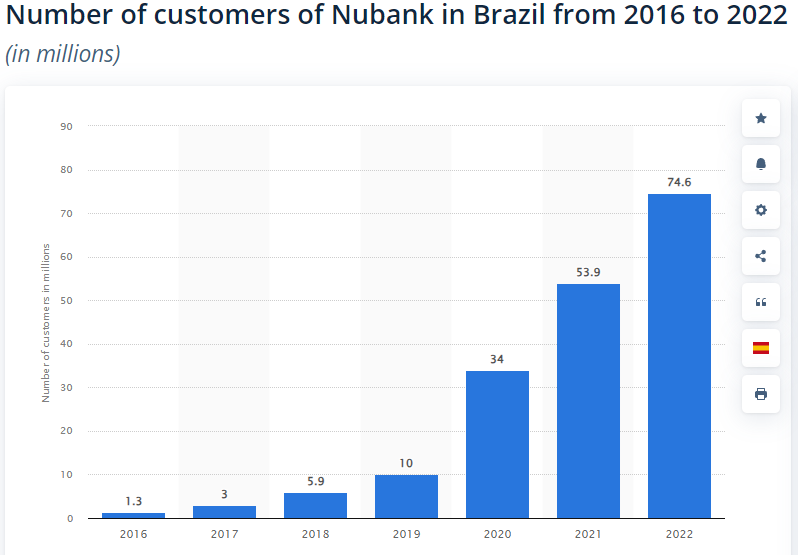

NU Holdings ($NU)

NU is one of the world’s largest digital financial services platforms, serving almost 94 million customers across Brazil, Mexico, and Colombia. While I was buying MELI heavily and analyzing the south American space for the stocks of interest, NU kept on popping up.

With over 100 million unbanked individuals in Latin America, Nubank had room to expand its customer base and market share and the customers have been commiting to the new bank.

The number of customers they managed to attract is astonishing.

The TAM it is growing into is massive which will protect growth for the mid-term.

Most investors I follow/ed in that space were long the name and finally Buffett bought it as well.

Despite the massive demand for this stock and the clear setup, I avoided it when comparing it with my other holdings. Additionally I was trying to avoid recent IPOs after the 2021/22 wreckage most IPOs had to deal with. Finally I was not a fan of banks as whole, missing the potential for NU to become more of a fintech name than traditional bank.

A miss to buy a good asset but also a miss the chance to further invest into the south-american space which I did well in in the past.

Robinhood Markets ($HOOD)

Following the 2020 craze and the GME induced hate the company has gotten, HOOD started its bottoming process, ranging from mid 2022 until last month or about 2 years.

Revenue grew 24% over the past year, assets have grown 65% and it managed to put in a positive net income quarter during the last period.

Overall the long base, the multiple contraction from 30 on IPO to a mere 5x EV/sales ratio in front of the breakout made it easy for HOOD to surprise positively. The massive hate towards the company makes it more interesting to me as well as we could see backwind should that view change in the future.

I was fully focused on Semiconductors this year which made me miss the trade/investment. I avoided it somewhat consciously as well to maximize my mental capital for the big semiconductor trades.

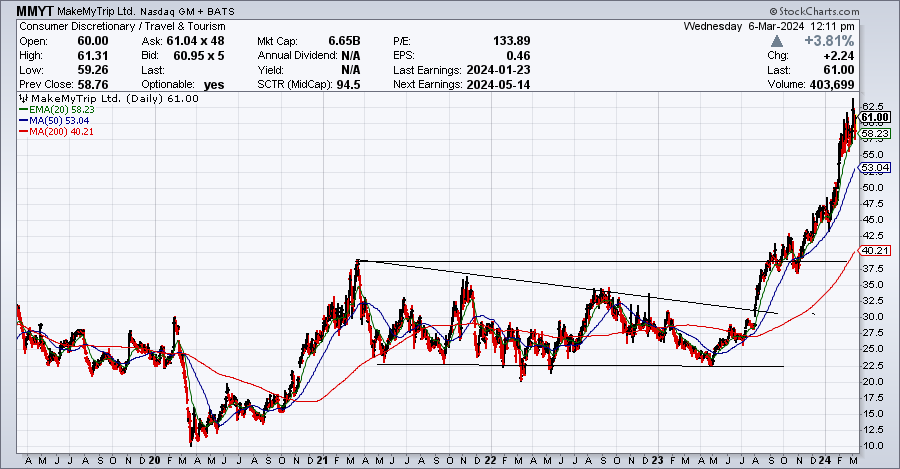

MakeMyTrip ($MMYT)

This is probably the one company on this list you will not know. MMYT is India's Nr.1 online travel agency and possesses a 56% market share. The company turned profitable in 2023 and is projecting strong growth going forward.

Alone the demographics in India as well as the economical growth make for a compelling backwind for a business that has in essence a monopoly in the online travel agency business.

Even better, MMYT provided a 2.5y base breakout to enter once it posted its Q1 2023 earnings (You will see the impact in the chart above). At a 6b market cap, the company has room to grow into the overall TAM.

This combination of fundamentals and the chart made for a great opportunity.

I missed this long, preferring bigger companies with more stable earnings. This is/was the ideal stock for small cap growth traders in my view.

Adobe Systems ($ADBE)

Adobe followed the same path as a lot of the tech stocks during 2022, crashing by over 60% while the Nasdaq drew down ~40%.

Despite the drawdown, Adobe showed resiliency by continuing to grow revenue by double digits per year. The net income dipped briefly, drawing down by a small 10% before reaccelerating into 2023.

Overall the technical setup Adobe presented was very similar to NFLX, but presented one distinct difference. While NFLX had a big empty gap to fill above, ABDE did not.

This gap mattered as we started our ascend. Contrary to NFLX and its unbroken rise, ADBE started its climb by failing the February 2023 breakout and retesting 325.

Shortly after in June 2023, the true breakout happened when we broke over the gap fill area set by the gap down in September 2022.

Since then ADBE regained new all time high net income and recently reached the 200ema for the first time since the bottom. Perhaps a good point to start a position or add?

It is hard to see this position as a very strong technical setup like many of the stocks in this blog, however the quality of the business itself made it more than adequate to start a long term position in my view.

Sequence: 350 breakout→ stopout→ 380 breakout→20ema ride→550 breakout→ 200ema retest

MongoDB ($MDB)

I first crossed paths with this company in 2020, when a developer debated about the use of MongoDB for a database project we had been working on.

‘MongoDB provides document databases using open source software and is one of the leading providers of NoSQL databases to address the requirements of unstructured data. MongoDB's software was downloaded 80 million times since 2009 and is frequently used for mobile apps, content management, real-time analytics and applications involving the Internet of Things, but can be a good choice for any application where there is no clear schema definition.’

MongoDB is a clear leader within this space, growing its revenue steadily from 100mil to 350mil since the Covid pandemic.

MongoDB reached a valuation of 9x sales near its bottom. To make you understand just how quickly the earnings grow, despite the nearly 3x since the bottom, the EV/sales ratio moved from 9x to 15x since.

The interesting thing about MDB is that most investors are not versed with the space. I believe engineers will know the company and simply use the tool. The word is not spreading as fast because of the buffer between the engineers and management. At least that is how I interpret why MDB is not talked about more.

Sequence: 250 breakout & 200ema reclaim→20ema ride→450 breakout→ recent fail and likely 200ema retest

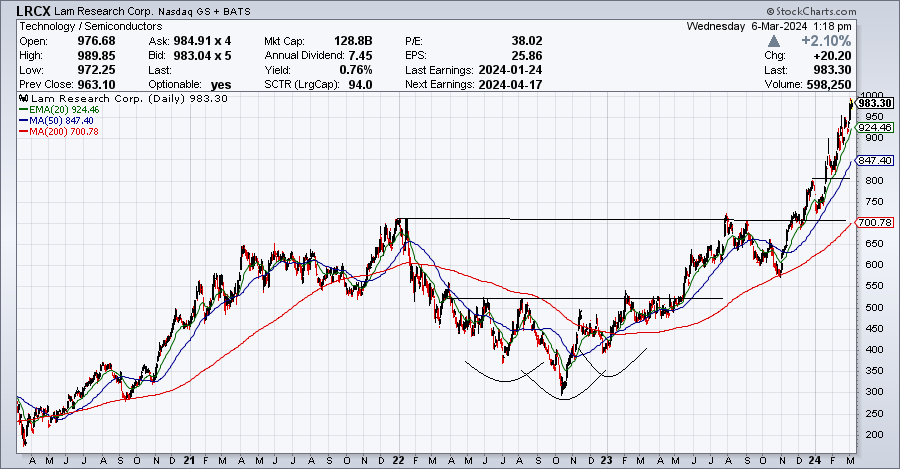

Lam Research ($LRCX)

LCRX was part of a select few Semiconductor stocks I was interested in during the bear market (AMD NVDA SMCI AMD LRCX AVGO).

Lam Research designs, manufactures, markets, refurbishes, and services semiconductor processing equipment used in the fabrication of integrated circuits.

LRCX was perfectly position to take advantage of the new AI age.

Its revenue and net income bottomed in 2022 when it started to top out. The combination of rising earnings and lowered multiples together with the new AI theme brewing made it the perfect candidate to take advantage of the the Semiconductor long.

More than just the fundamentals, LRCX had an exquisite setup.

LCRX formed an inversed head and shoulder, resolving higher while reclaiming the 200ema and hugging the 50ema to breakout higher forming a right shoulder penant.

The management was simple. A powerful setup followed by a 20ema ride, a 200ema retest followed by an all time highs breakouts and 20ema powertrend.

Sequence: Head and shoulders + right shoulder penant + 200ema reclaim + 50ema ride breakout→ 20ema ride→ all time highs test→ 200ema retest→ all time high breakout→ 20ema ride→ breakout and repeat

Broadcom ($AVGO)

This is one of my biggest misses ever. I had heard of AVGO before and understood they were a leader.

Broadcom Inc. designs, develops, and supplies various semiconductor devices with a focus on complex digital and mixed signal complementary metal oxide semiconductor based devices and analog III-V based products worldwide. The company operates in two segments, Semiconductor Solutions and Infrastructure Software.

Contrary to LXRC, the revenue never declined and the market bottom gave us the green light to start catching up higher as net income recovered(margins 10% to near 40% now).

The setup started by reclaiming its 200ema and breaking out of a yearly down trending trendline.

The trend was clear from there, riding the 20ema and 50ema all the way into a massive breakout which almost doubled the stock. Instead of finishing its move there we built a 6months consolidation and broke higher before continuing the trend even more aggressively with the 20ema.

Given the AI theme and the beautiful trend, this was an easy setup to take advantage of and one of the most quiet big trade out there since the 2022 bottom given its almost 400% run.

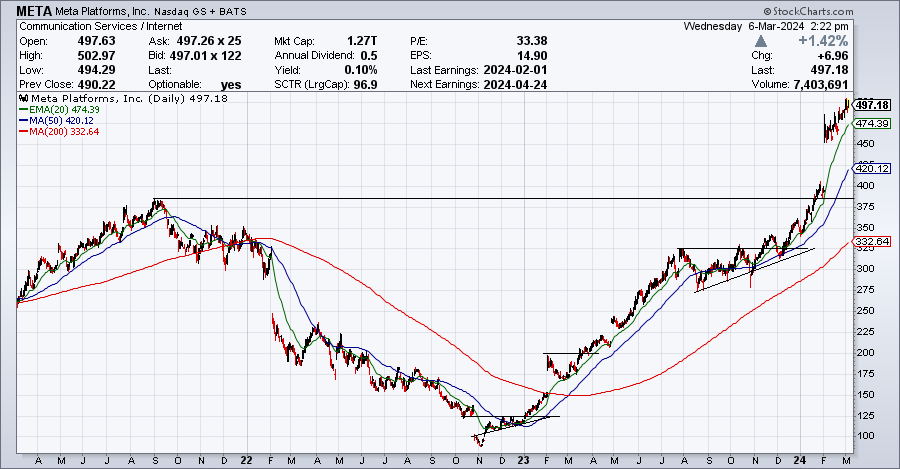

Meta Platform Facebook ($META)

How could this list be done without Meta. Faceboo got crushed in 2022 following their spending extravaganza into the metaverse, drastically accelerating their expenses.

Towards the bottom drastic changes got made. First META would stop the spending spree in the metaverse and also proceed to have layoffs. This cost control which we had not seen from Facebook since the top was finally back.

This provided us with a clear Risk-reward and catalyst to initiate a long term position or at least a trade. I understood the news and the contra-consensus positivity being METAs management decision, however I was busy with NFLX and missed the entry, missing the bigger picture idea.

On a personal note, I do not use Facebook and I do not know anyone but marketers that use it but this is short sided. Individuals outside of the most developed countries as well as older individuals are still using Facebook and the earnings were showing it.

This personal opinion and general consensus made it even more interesting of a trade, leading to the consensus shift and longer acting bid through it if we turned.

Sequence: gap fill breakout(with catalyst)→ 200ema reclaim + EP setup→ breakout→ 20ema ride→ Wedge breakout(+50ema ride)→ All time high breakout→ EP setup breakout

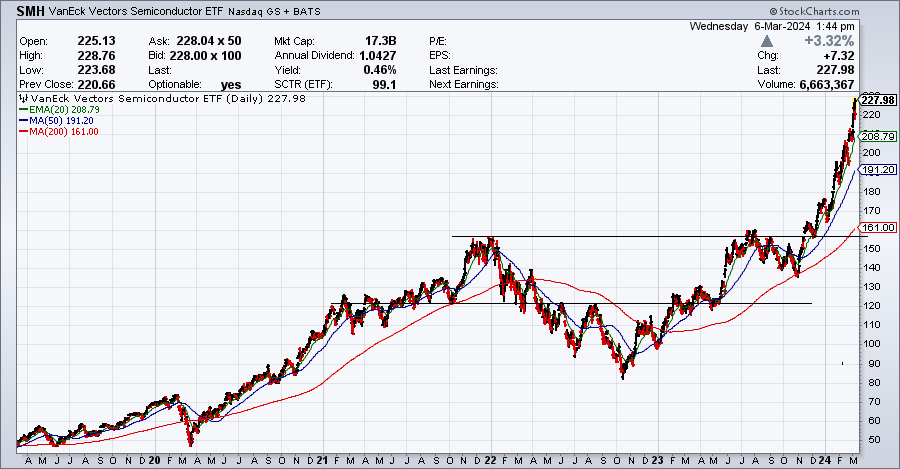

Semiconductor ETF (VanEck Vectors $SMH)

To end this blog, we will look at SMH. To me this was the easiest way of all to partake in the Semiconductor bull market. We got a clear 200ema reclaim and inversed head and shoulder to start this trend, followed by a cup and handle on the all time highs to add or initiate a position.

Since the breakout we have been riding the 20ema for 50%+ in a few months.

I was busy with my holding and the massive rise of my portfolio at the time and simply did not commit capital to this easy and logical trade.

Sequence: Head and shoulders + 200ema reclaim→ 50ema ride→ Cup and handle (all time highs)→ 20ema ride

All in all

I hope you have enjoyed this recap of the best opportunities I have missed following the market bottom in 2022/23. Reflecting on these is important to make sure to be prepared for the next instance and market crash.

Overall despite all the misses above, I managed to compound the account by about 120% during 2023, outperforming major indices and most stocks as well.

Hopefully the next time I do such a recap, I will have no tickers on my list.

Great read, cheers for sharing.

When you are differing between an investment and a technical setup, what sort of analysis will you want to do before investing in a company versus a mid time frame trade? Do you do your own DCF work / look at any main metrics such as roic/management team/multiples?

Keep up the good work

Hell yeah Lukas